In March Lendinvest reported a surge in loan originations and had an exceptional month with more volume originated than Ratesetter or Funding Circle. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in March 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month

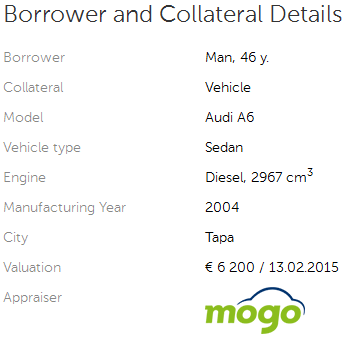

Today Latvian Mintos expanded by now offering loans to Estonian borrowers on the p2p lending marketplace. These loans are secured with a car as collateral. Today 15 loans were posted on the platform. Typical (nominal) interest rates for these loans seem to be between 11 and 13%. LTVs are as of today in a wide range from 26% to 90%.

CEO MÄrtiņš Å ulte told P2P-Banking.com: ‘From today we also offer investors opportunity to invest in loans secured by vehicle. We provide these loans in cooperation with Mogo (http://mogofinance.com), the market leader in car loans with operations in Latvia, Lithuania, Estonia, and Georgia. … as part of our international expansion we have set up a company in Estonia and are working on entering Lithuania and Poland to boost our loan origination capacity‘. Continue reading →

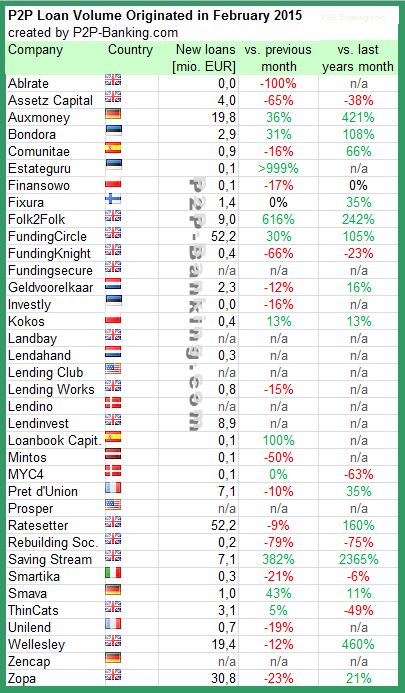

As February was a shorter month, loan originations fell compared to January with some exceptions. Ratesetter and Funding Circle are in a neck-and-neck race for largest volume figure this month. Prosper and Lending Club no longer publish origination data for the most recent month. I added two more services. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in February 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations.

P2P lending service Bondora, headquartered in Tallinn, announced that they raised 5M US$ Series A round led by Valinor Management to fuel further expansion plans for cross-border lending in Europe. Richard Fay and Ragnar Meitern also invested. Bondora was the first p2p lending service doing cross-border lending for retail investors. Bondora is currently facilitating loans to borrowers in Estonia, Spain, Finland and Slovakia from investors in all European countries. Bondora states that investments on the marketplace have consistently yielded premium returns to investors while simultaneously delivering competitive rates to borrowers through efficiency and lower interest rate spread.

Uniting European markets under the roof of a single platform creates a huge opportunity given the size of the population in the continent and the volume of outstanding debt. Thus, Eurozone countries alone account for 340 million people and EUR 1.1 trillion in outstanding consumer credit debt, a market equivalent to US. Lending to borrowers in markets that are independently relatively small (even Germany, the largest economy in Europe is only approximately twice the size of California in terms of GDP) allows earning premium returns due to lack of competition among traditional lenders.

Pärtel Tomberg, CEO and co-founder of Bondora, said he hoped the cash infusion from Valinor Management, the hedge fund run by David Gallo, will allow his company to build the more complex infrastructure needed to make more cross-border loans. ‘The goal is really to become a global market,’ Pärtel Tomberg said in an interview. ‘There are no precedents in the world on many of the things we want to do.’

The company also wants to attract institutional lenders from the US.

A possible mid-term competitor might be Lending Club. But Lending Club said in the investor conference call on Tuesday that they will focus on the US market and will not use the capital raised in their December IPO on international expansion plans in the near future. Renauld Laplanche is however monitoring international developments in the market: ‘We’ll see what model is really the winning model in any particular geography.’ Continue reading →

Estonian p2p lending marketplace Investly announced that Sonny Aswani became an investor. He will invest also directly in the loans offered via Investly. Continue reading →

Recently launched p2p lending marketplace Mintos is in disagreement with a consumer right protection body of the government over the interpretation of rules regulating lending to consumers and whether Mintos is conducting business within these rules or not.

Two statements were published on the internet (here and here) last Friday that state, that while Mintos has the necessary license to lend to consumers, it failed to mention during the application that it would receive deposits from third party investors and make assignment of loan parts to these investors, for which in the view of the PTAC it lacks the necessary license. In the statement the body asks Mintos to cease continuing with this practise.

P2P-Banking.com contacted Mintos CEO MÄrtiņš Å ulte on Friday evening and received this comment by him: ‘To put it shortly Consumer Right Protection Centre (CRPC) has asked us to provide additional information on how peer-to-peer process works at Mintos. Before launching Mintos we did an in-depth legal due diligence and we are confident that we are working in accordance with all aplicable regulations. The peer-to-peer (or better, marketplace) lending is still nascent industry and regulators in general around Europe are still debating on how to best respond to it. As forerunner of peer-to-peer lending in Latvia we have already had discussions with regulators and will continue to engage with them and help with information where necessary. We will hold an official press conference on Monday to encourage further discussion.‘ Continue reading →