On October 1st Jevgenijs Kazanins became new CEO of Latvian p2p lending marketplace Twino. He previously worked as CMO at Estonian p2p lending marketplace Bondora. Twino was launched in June and is part of the Finabay group which operates since 2009. So far all loans offered on the p2p lending marketplace are from Latvia, whereas the Finabay group is active in a broader set of markets. Twino is open to international investors – German retail investors are the largest foreign investor base.

In a call with P2P-Banking.com the new CEO outlined the expansion plans. Twino will add loans from new markets, starting with polish loans shortly and possibly adding loans from countries like Russia, Denmark or Georgia at a later stage. There will be no currency risk for investors as it will be covered by Twino. Twino will apply its buyback guarantee to all loans – by which Twino covers overdue principal and interest for investors once a loan is 60 days overdue (though due to extensions this might take 8 month). The interest rate offered to investors for p2p loans in the new markets will be in line with the current offering: up to 14.9%. The loan terms will likely longer and Twino will move away from the current very short term loans many of which I deem essentially payday loans. He said: ‘… we are working on introduction of the loans from other markets, where Finabay has lending operations, such as Poland, Russia, Georgia and Denmark. The reason for the inclusion of other countries is that the demand from investors has already surpassed the volumes we can originate in Latvia. We aim to offer similar rates to the Latvia-originated loans and all loans will also come with the buyback guarantee‘

Since the mother company Finabay is already originating these loans, it will not be a challenge to build loan volume. Kazanins aims to originate 5 million Euro loan volume per month. As the loans already exist and the new aspect consists only of refinancing through p2p investors, Kazanins is convinced of the good quality of the loans: ‘We estimate that 15-20% of [polish] loan volume will be bought back through the BuyBack Guarantee program (defaulted loans and loans with more than 6 extensions‘.

Twino also works to add statistics to the site. He stated: ‘ … Disclosing information about financial health of Finabay is highly important given the fact that all loans offered on the platform come with the buyback guarantee …‘

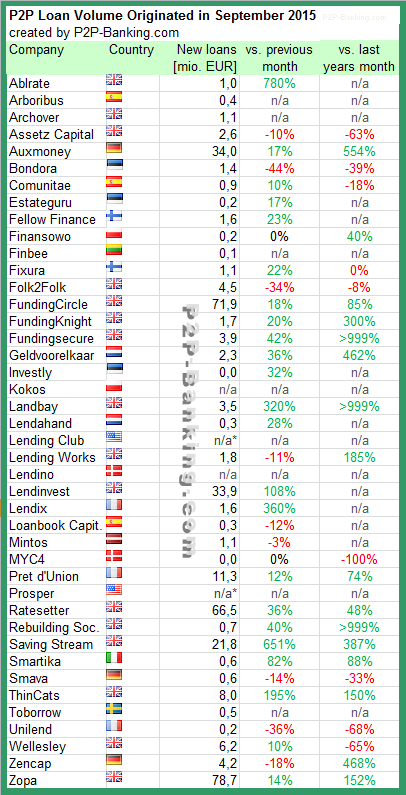

The following table lists the loan originations for September. Most marketplaces grew their loan volume compared to the previous month. Saving Stream had an exceptional month, with several very large loans. I added 4 new services to the table. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in September 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Mintos is a marketplace lending platform that brings together investors and borrowers by enabling various loan originators to use a marketplace lending model in funding loans. Previously loan originators established their own platforms; now Mintos offers a single platform to those non-bank lenders that seek to sell loans. This means non-bank lenders do not have to make major investments in establishing and maintaining their own platforms. By connecting to the Mintos platform non-bank lenders get an instant access to investors that are looking to purchase marketplace lending assets. Thus, non-bank lenders can focus on their core skill of originating loans.

What are the main advantages for investors?

At Mintos investors can invest in loans that are originated by various non-bank lenders that use our platform to fund their loans. The main advantage for the investors, accordingly, is that they get an access to much broader investment opportunities as part of a single platform, both in geographic terms, and in terms of various loans originated by various non-bank lenders. Investors on the Mintos platform can invest in mortgage loans, secured car loans, small business loans, and soon also unsecured loans. Loans are currently originated in Estonia, Latvia, Lithuania, and we are about to add loan originators from Finland, Georgia, and Spain. This, combined with the fact that the minimum investment in one loan is EUR 10, means that investors can easily build very well diversified investment portfolios. Also, as a result of having various loan-originators and many investors on one platform our secondary market is very liquid.

It is also important that non-bank lenders whose loans are available to investors on our platform are experienced in underwriting. The platform is used by Capitalia, for instance, which is the leading small business lender in the Baltic sates and has been lending for five years. All lending processes are orderly at the company, it has experience, and it has access to historical data. That is essential for investors who can be sure that the detailed credit analysis are preceding the granting of a loan. Moreover, the loan originators on the Mintos platform are required to retain a part of each loan on their books, i.e., to have “skin in the game†to align their and investors’ interests.

Finally, all loans on the Mintos platform are prefunded by the loan originators; thus investors can start earning from the moment of the investment and there is no cash drag. At the moment more than EUR 1 million of loan inventory is readily available for investment on our platform.

What about borrowers? What are the advantages for them?

Mintos does not issue loans, but it is important for us that the loan originators who use our platform at the end of the day can offer cheaper rates to borrowers. Also, the lending process is much more convenient at these loan originators. When borrowing money from Capitalia, for instance, a small company can expect the money to arrive in its account in just a few days’ time, usually even faster. At a bank, by contrast, that could take several weeks. Finally, some of the loan originators who use our platform provide loans and services to those borrowers who might not have had an access to affordable credit before. For instance, among clients of Mogo, the largest non-bank car loan provider in the Baltic region that is also on our platform, there are those who are seeking a car loan, with the average requested sum being around EUR 3,000. This segment is underserved by the banks.

What ROI can investors expect?

So far the average net annual return for investors investing via the Mintos platform have been slightly below 13%. We expect the average net annual return to hover around the low double digits also in the future. However, investors should look not just at the return, but also the relevant risks. In the case of Mintos, investors can easily build a very well diversified investment portfolio across different loan products and geographies, thus reducing unsystematic risk within the marketplace lending asset category. Also, the Mintos platform was the first with a buyback guarantee where some of the loan originators buy back non-performing loans from investors, thus substantially reducing risks for investors.

What is the background of Mintos?

We started to work on the idea in mid 2014 and launched the platform in January 2015. I come from the investment banking where I spent six years before going for an MBA at INSEAD. That, actually, was the first time I heard about the peer-to-peer lending because I borrowed from Prodigy Finance, a platform that provides funding to international postgraduate students attending top-ranked business schools, while also delivering competitive financial returns to institutional and private investors. The other Martins, Martins Valters, our CFO and also a Co-Founder, has 11 years of experience from Ernst & Young where he audited some of the largest financial institutions in the Nordic region.

To fuel our growth we have raised EUR 1 million in venture capital to date. That has helped us in forming a strong team and an experienced board of directors. In a bit more than six months since the launch, more than 2,400 investors from 30 countries have registered on the Mintos platform and funded more than 1,500 loans for a total of more than EUR 4 million, of which EUR 1 million in the last month alone.

Is yours a bespoke platform?

Yes. We began work on the platform half a year before we launched it to the public, and we developed it in-house from scratch. Each marketplace lending platform has its own nitty-gritty approach, so it is best to design the platform ourselves. The Mintos platform is used by various non-bank lenders, and so we see ourselves as a technology company with a strong finance background. Currently, we have eight software developers in our team. We listen carefully to what investors say and appreciate their feedback as it greatly helps in improving the platform. Continue reading →

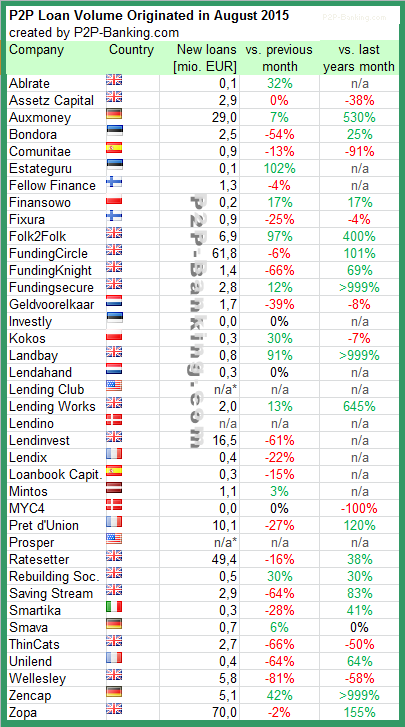

The following table lists the loan originations for August. August was a slow month for many of the listed services probably due to the holiday season. Zopa crossed 1 billion GBP lent since inception (see infographic) and Giles Andrews stated he expects the next billion to be lent in 2016. I do monitor development of p2p lending figures for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in August 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

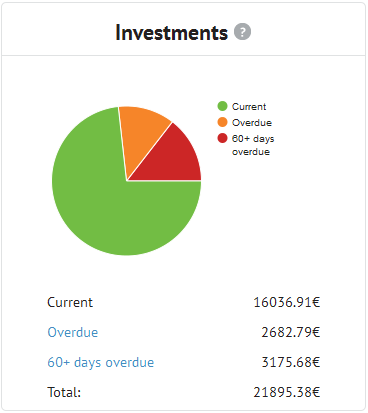

In October 2012 I started p2p lending at Bondora. Since then I periodically wrote on my experiences – you can read my last review published in April here. Since the start I did deposit 14,000 Euro (approx. 15,900 US$). My portfolio is very diversified. Most loan parts I hold are for loan terms between 36 and 60 months. Together the loans add up to 21,895 Euro outstanding principal. Loans in the value of 2,683 Euro are overdue, meaning they (partly) missed one or two repayments. 3,175 Euro principal is stuck in loans that are more than 60 days late. I already received 15,202 Euro in repaid principal back – this figure includes loans Bondora cancelled before payout. I reinvested all repayments.

Chart 1: Screenshot of loan status

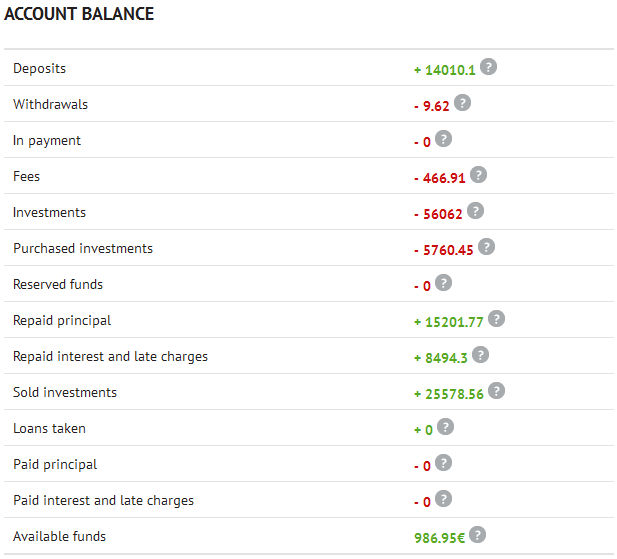

At the moment I have 0 Euro in bids in open market listings and 987 Euro cash available.

Chart 2: Screenshot of account balance

Return on Invest

Currently Isepankur shows my ROI to be 26.76%. In my own calculations, using XIRR in Excel, assuming that 30% of my 60+days overdue and 15% of my overdue loans will not be recovered, my ROI calculations result in 21.8%.Continue reading →

Laimonas Noreika is the CEO of Finbee, a p2p lending service that launched last week and is open to international investors starting today.

What is Finbee about?

FinBee is about borrowing for less and earning more when investing. We also are most user friendly p2p lending platform in Lithuania.

What are the three main advantages for investors?

Firstly, our loans have high interest rate – from 10 to 40 percent. That means, that investor can expect higher return of investment, compared to other p2p lending platforms. Secondly, we have reliable software, that is developed by UK based Madiston. That means, that it is tested and extremely user friendly from day one. And finally, we pay great attention to selection of borrowers, so that the risk for investors is minimized as much as possible. On top of that, we invest 10 percent on total sum into each and every loan, so we share the risk with investors. In the near future we also will introduce compensation fund that in an unlikely case of borrower defaulting on its loan will compensate lenders their investment.

What are the three main advantages for borrowers?

I would say that first and foremost, we offer cheaper loans than most of the players in Lithuanian market, including banks, payday loan companies and credit unions. This is achieved by implementing auction principle when borrowing. That means, that borrower can set interest rate ceiling, for example 15 percent. Lenders then are able to offer lower interest rate, therefore making loan interest rate for the borrower as little as 12 or 13 percent. This is free market at its finest, when the market sets the real interest rate for the benefit of the borrower. Secondly, we are very consumer friendly. We talk, look like and do our business like majority of our clients. We know, what they want and we are doing our best to meet those expectations. Lastly, we have a fair commission policy. That means that if borrower has high credit rating, our commission is lower.

What ROI can investors expect?

It‘s all up to investors. Loan interest rate will be between 10 and 40 percent, therefore investors can decide for themselves if they want lower risk and lower potential ROI or higher risk with possibility of higher potential ROI.

How did you start Finbee? Is the company funded with venture capital?

FinBee started little over a year ago, when I quit my position as a CMO in one Lithuanian company and started everything from scratch: examining the market, getting know-how, attracting investors and partners, picking up experienced team members. Big breakthrough moment was when Madiston became our partner and we got a technological edge against our local competitors

Is the technical platform self-developed?

No, software is provided by Madiston, whose Tim Simon is also member of FinBee board. Tim has an extensive experience of delivering successful applications to the Financial Technology marketplace as a founder and CEO of Quotient plc and Mondas plc, listed on the London Stock Exchange and AIM respectively. Continue reading →