Marketinvoice and Platform Black have offered the possiblity to invest in invoice finance / invoice discounting loans for some time in the UK. However these were not an option for me due to requirements (minimum invest and/or UK bank account).

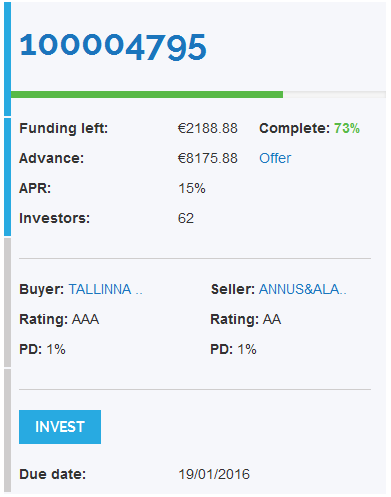

Therefore I made my first bid on a loan of this type on Investly on Dec. 31st. It was the first invoice discounting loan the Investly marketplace launched, making this asset class available to investors in the European Union from bid amounts as low as 10 Euro. Investly ran the offer in a three day auction period, with 15% maximum interest. Even though the bidding period was over New Year, the demand was high and several investors were outbidded during the underbidding auction (screenshot right shows status on first day of auction). Registered investors are able to see the underlying invoice that is financed.

The loan is for less than a month, due to be repaid on January 19th.

Today Mintos launched a cooperation with DEBIFO which as a originator will provide invoice finance loans on the Mintos platform. That enabled me to make my second bid in invoice financing. The loans listed today at the Mintos p2p lending marketplace carry interest rates from 11.2% to 13.8% and are for a loan term of less than a month.

‘For most of the small and medium enterprises in the Baltics, receiving client payments in time is critical in order to ensure continuous operations. While many of these companies have large, reliable and stable business customers, they typically set payment terms of up to 60 days or more, which makes it hard for small businesses to survive’, says the peer-to-peer lending platform Mintos CEO Martins Sulte, who welcomed the cooperation with DEBIFO.

Mintos management forecasts high investor interest in this investment product. Martins Sulte continued by saying ‘Most of these outstanding invoices are from stable, large companies, which means that the risk is relatively low. The other aspect that investors will like are the short repayment terms’.

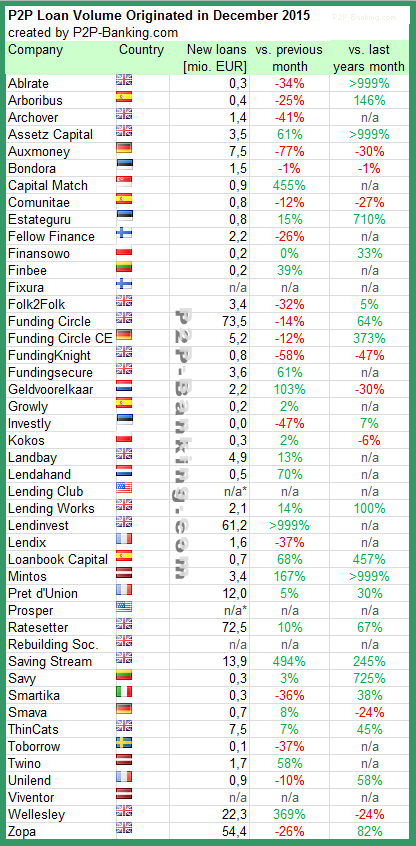

The following table lists the loan originations for December. This month Funding Circle led slightly ahead of Ratesetter. Funding Circle UK also crossed the milestone of 1 billion GBP loans originated since launch. I added two more platforms to the list. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in December 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

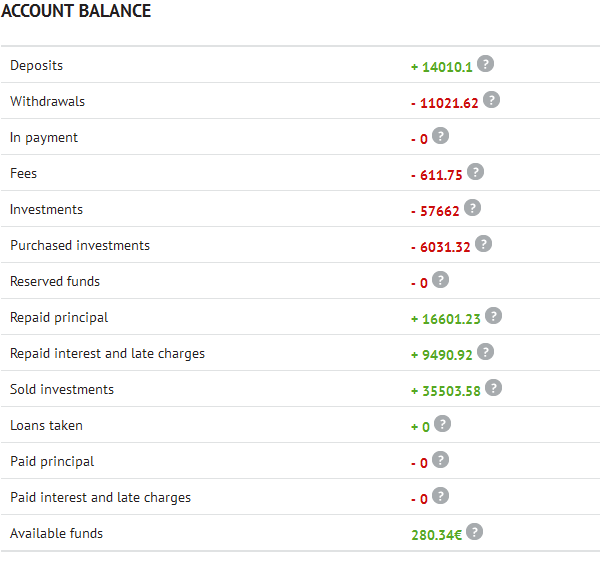

In October 2012 I started p2p lending at Bondora. Since the start I did deposit 14,000 Euro. Since then I periodically wrote on my experiences – you can read my last review published in August here. In the 4 months since then, many changes happened at Bondora: New portfolio manager, new dashboard view, new collection procedures, a first version of an API in production, no more transaction fees for buying and selling on the secondary market and Bondora now allows investors to sell and buy defaulted loan parts (60+days overdue). I used this change to sell my overdue Slovakian loans at 87% discount. I also sold my remaining Spanish loan parts. I did not have much of either of these in my portfolio anyway.

I also reduced my overall portfolio position at Bondora and transferred 11,022 Euro back to my bank account. I managed to sell many of my Estonian loans at a premium. My perception is that the liquidity on the secondary market increased after the transaction fees were removed. Still it is hard to effectively navigate on the secondary market.

I find it hard to price 60+days overdue loans I want to sell on the secondary market. The site Bondpicking.com has charts with recent transactions for defaulted loan sales on the secondary market that can help as guidance.

Currently I still have loan parts with the value of 11,428 Euro outstanding principal. Of these 1,441 Euro are in loans that are overdue and 2,076 Euro are in loans that are 60+ days overdue.

At the moment I have 280 Euro cash available.

Chart 1: Screenshot of account balance

My interim conclusions after 3 years

I am very satisfied with my Bondora investment. Of the 14,000 Euro investment I already withdrew over 11,000 Euro, meaning my remaining risk (concerning the initial investment) is very limited and I still have a huge portfolio of loans. Currently Bondora shows my ROI to be 25.0%. In my own calculations, using XIRR in Excel, assuming that 30% of my 60+days overdue and 15% of my overdue loans will not be recovered, my ROI calculations result in 16.3%. Even in a very pessimistic scenario adding up only withdrawals (approx 11,000 Euro), current loans (about 8,200 Euro) and cash (280 Euro), the initial 14.000 Euro grew in three years to a value of 19,500 Euro. Continue reading →

We have created what is best defined by the term “bankâ€. But our bank is virtual; it differs from a traditional one in that it is exempt from the requirement of capital sufficiency. Borrowers apply for loans and investors grant loans on our platform; it’s a meeting place.

In short, the SAVY P2P lending platform is a virtual bank that (will) operate in three segments:

Consumer credits, that is, personal loans;

Loans with real estate mortgage (for persons and businesses);

Business loans.

We have not yet offered business loans; however, we are planning to offer the service by the end of 2016. Our real estate product will be fully launched by the end of this year. Our secondary market appeared in early 2015.

A standard practice of global P2P lending platforms is that investors transfer funds to an account owned by the platform managers and the latter do the lending. We took a different path. The SAVY interpersonal borrowing platform does not manage the funds of investors directly. Each investor creates their own “personal wallet†in the Paysera e-money institution. They are then entitled to use their funds at their own discretion; for example, they can take their money out as soon as they need it without any intervention from SAVY. Even theoretical risks for investors’ money are eliminated under this structure. The platform reserves the right to evaluate the creditability of borrowers and allocate investors’ money to the borrowers. Other risks, such as funds being used for other purposes than intended by investors, are simply impossible on our platform. Paysera is an e-money institution. Investors can be confident as Paysera has 10 years of experience as an e-money license holder in the European Union. Its business in Lithuania is supervised by the Bank of Lithuania.

What are the three main advantages for investors?

Safe storage of money. The platform does not manage any investor funds. The funds are kept in dedicated e-accounts of each individual investor. In addition, investors are not charged a fee for investing their capital on the platform.

Experienced team. All members of our team and management are experts in their respective fields of business. This is very important in this new, dynamic industry.

Possibility to diversify risks. Traditional platforms offer only a single product for their investors. SAVY (will) offer the ability to invest across three different sectors and risk types on one intuitive system.

What are the three main advantages of SAVY platform for borrowers?

The SAVY platform is a new alternative for borrowers, something that has never before existed in Lithuania. This is a speedy and cost effective solution compared to expensive payday companies, banks and credit unions.

Our platform offers borrowing costs at a price similar to bank credit cards or even cheaper.

We guarantee a quick loan. Furthermore, we do not impose any fees on early repayment.

What ROI can investors expect?

Currently, the average return on investment is over 20 percent. Generally, our investors should plan a net return somewhere between 15 and 20 percent for the unsecured product loans. For the secured loan products such as real estate and business loans, they can expect slightly less. The expected return on investment for foreign investors on platforms from Central and Eastern Europe is, generally, much higher than the same metric found on Western European platforms.

What is the background of the SAVY team?

Our team is a collaboration of industry professionals, which is crucial to create an innovative and effective product in the financial sector. For example, our marketing manager is the former general manager of one of the largest Lithuanian consumer credit institutions. We have an internal lawyer with an MA degree in Law from a prestigious university in the UK, who is also a former employee of a private capital fund there. We have a banking professional on our board, well known in the Baltic region, and former CEO of SEB and Å iauliu Bank in Lithuania. An American professional in commercial real estate development is also on our team. […] Continue reading →

The following table lists the loan originations for November. Funding Circle overtook Zopa measured by new volume followed by Ratesetter. I added two more platforms to the list. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in November 2015. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Lithuania will regulate p2p consumer lending starting February 1st, 2016.

The main requirements introduced by the new legislation in Lithuania are:

40K Euro of share capital required by the marketplace company,

contingency plan in case of failure of the platform,

limitation of 500 Euro investment per one loan,

limitation of 5,000 Euros investment per platform for ‘inexperienced’ investors,

marketplaces will be allowed to gain their revenue only from monthly instalments paid by borrowers. This means that all platforms will not gain revenue if their portfolio is not performing.

Laimonas Noreika, CEO of Lithuanian p2p lending company Finbee told P2P-Banking.com: ‘Once again Lithuania proved itself as a country with strict financial regulation. [The] new law gives more transparency to all – lenders, platform owners and public authorities. FinBee welcomes the regulation and invites international lenders to discover Lithuania as a country open for P2P lending.‘ Continue reading →