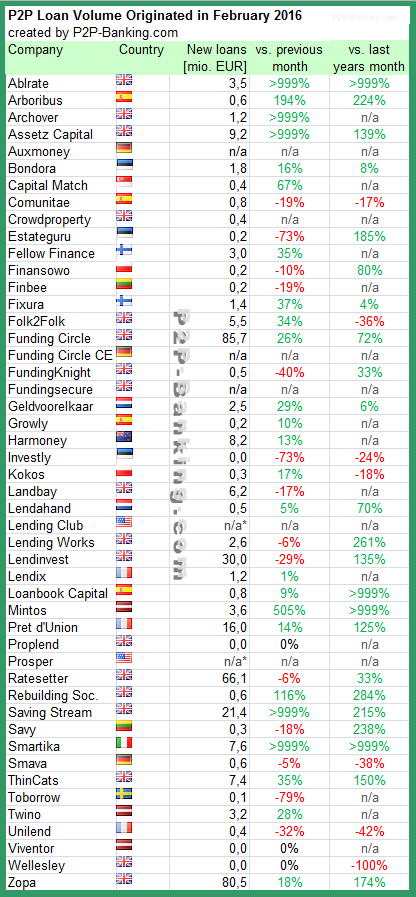

The following table lists the loan originations for February. Funding Circle leads ahead of Zopa and Ratesetter. I added Harmoney and Crowdproperty to the list. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Smava reached 100M EUR (counting p2p loans only, not the brokerage model for banks) since launch

Table: P2P Lending Volumes in February 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Latvian p2p lending marketplace Mintos has raised 2M EUR from VC Skillion Ventures in Riga. The p2p lending service was launched a year ago and lists loans from several loan originators. The loan types include mortgage loans, secured car loans, business loans, personal loans and invoices finance. The majority of the retail investors resides in Latvia, Germany and UK.The investors financed a cumulative loan volume of over 16M EUR since launch.

The loans are currently to borrowers in Latvia, Estonia, Lithuania and Georgia. Mintos CEO Martins Sulte plans to add loans in the markets of the Czech Republic and Poland next. Continue reading →

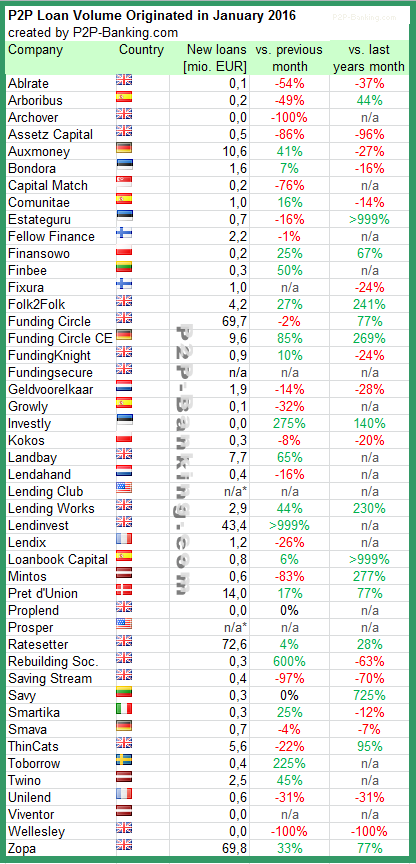

The following table lists the loan originations for January. This month Ratesetter led, followed by Zopa and Funding Circle. I added one more marketplace to the list. I do monitor development of p2p lending statistics for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services.

Table: P2P Lending Volumes in January 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

Tallinn based p2p lending marketplace Investly, which recently launched an invoice finance product in Estonia announced the launch of the service for UK SMEs. The invoice finance option will give UK businesses almost instant access to much needed working capital to aid growth.

The launch comes after a successful European launch of the platform in Estonia 18 months ago, and a subsequent investment of 600,000 Euro from Venture Capital group, SpeedInvest.

Until now, invoice finance options – whether through traditional channels or via other peer-to-peer platforms – have been complex and laden with fees and charges.

Investly says it has simplified the product so that, once credit checks have been cleared, SMEs can sell invoices to investors within two days. And therefore assign the money to aid growth, enabling them to be the best they can possibly be without the cash flow worries. Initially, the invoice finance product will be available to any UK SME who passes the platforms sign-up criteria, which includes credit checks and confirming their identity. Further safeguards are put in place such as directors’ checks and potential guarantee.

Ruth Chamberlain, Investly’s UK Country Manager, said: “Long payment terms are crippling for UK SMEs. They are dependent on cash to sustain and grow their business, but as they invest in products and people, they may not get money on work completed a month or even 120 days after issuing their invoice. This is putting many businesses at risk – especially smaller ones and those that depend on payments from one or two key customers.†Continue reading →

I started investing in loans on the Latvian p2p lending marketplace Mintos right after it launched 12 months ago. At that time Mintos offered real-estate secure loans only. The service has evolved hugely with a much wider range of loan types on offer now. Mintos now serves as a platform to enable the transactions while partnering with loan originators, who actually originate loans and are responsible for vetting the borrowers.

Overview of the current main parameters for investors:

Different loan types

Typical interest rates range from about 8% to about 14%

0% fees for investors on the primary market (1% seller fee on the secondary market)

All loans prefunded; investors earn interest from the day they invest money into a loan

Depending on the provider, some of the loans offer buyback guarantees; that means if the loan becomes more than 60 days overdue the provider will pay the principal and the interest of that loan to the investor

Open to international investors

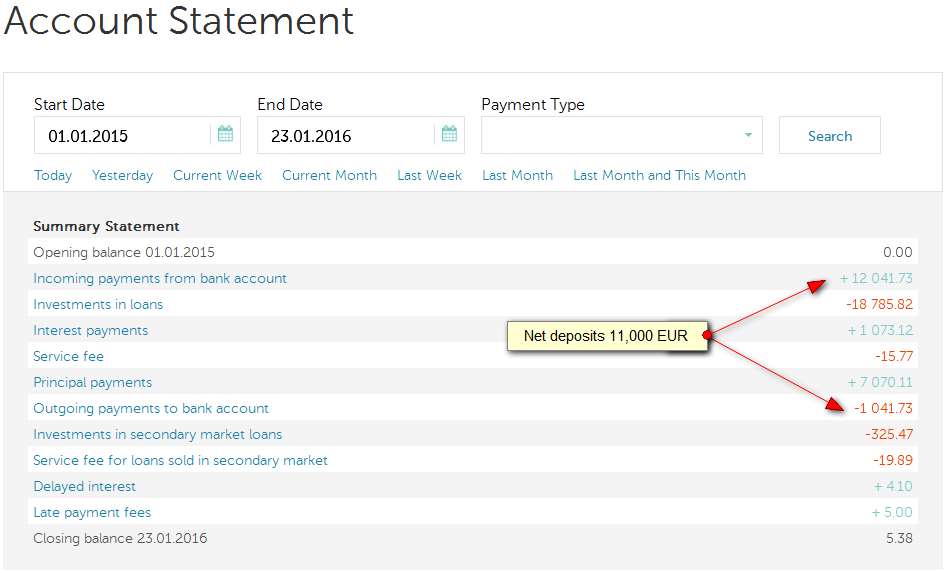

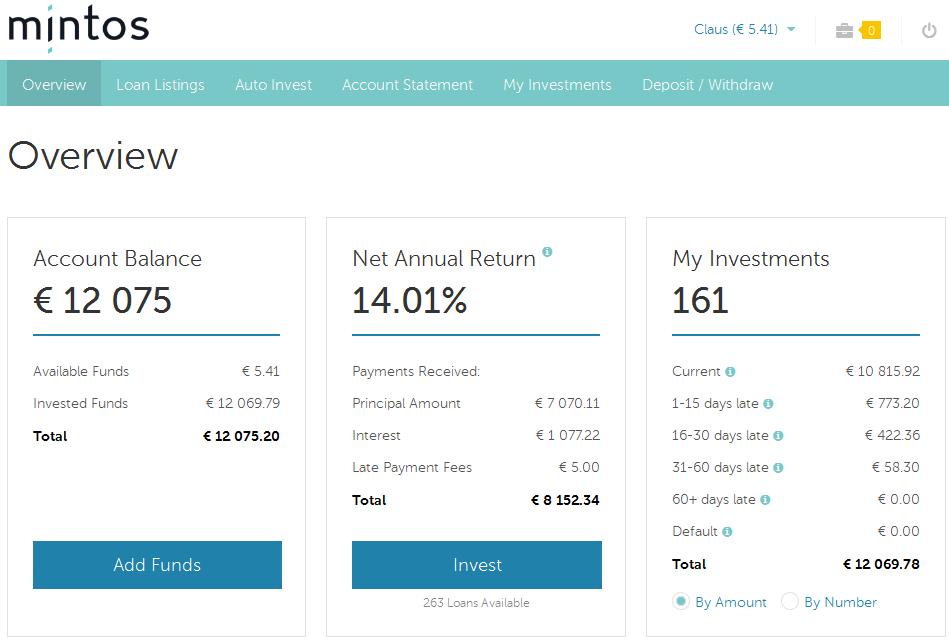

During the past year in several installments I deposited 11,000 Euro into the account via SEPA transfer (actually I deposited 12,041 Euro; but I also withdrew 1,041 Euro). Deposits are fast and reliable; they usually took less than 1 business day for me. Most of the time, I reinvested all repayments and interest earned.

My portfolio yielded 14% ROI so far

Currently I have 12.069 Euro invested in 161 different loans. Over 70% of the amount is in Mogo secured car loans (with buyback guarantee). Over 20% is in mortgage loan (without buyback guarantee). The remainder is in business loans and invoice finance loans (mostly without buyback guarantees). I stayed clear of the personal loans Creamfinance originated in Georgia. The shown 14.01% are an accurate reflection of the actual ROI, I believe. Continue reading →

Viventor is about providing sensible investment opportunities for investors from all over Europe. As we started considering the idea of Viventor less than a year ago, peer-to-peer financing was achieving remarkable success in the US and the UK. In contrary, the “old continent” was relatively underserved.

And so the goal was set – to build a peer-to-peer lending platform for European investors that is accessible, makes investing convenient, and offers high quality services, investment opportunities, and the product itself.

What are the three main advantages for investors?

Firstly, it is the investments themselves. All loans currently offered are secured by liquid real estate mortgages, as well as come with Buyback Guarantee. The weighted-average LTV ratio of our loan book is 28.45%, and we are proud to be the market leaders in terms of providing such low-risk opportunities.

Secondly, the investors receive fixed monthly interest payments. Relatively few platforms do this, but we see it as an advantage for the investors. Instead of diminishing interest and trying to crack advanced formulas, we offer straightforward logics and exactly the same payments every month. We want to make investing convenient also for people relatively unfamiliar with the world of finance and peer-to-peer lending.

Thirdly, it is the simplicity and convenience of investing. We are constantly making efforts towards removing the friction from the investment process itself by building the platform and its UI simple and intuitive for any user. Improvements based on everyday findings are constantly implemented, new languages are added, and educational material is made available. Our aim is to for investing to be simple and enjoyable.

What are the three main advantages for borrowers?

Viventor does not originate loans itself, and this is unlikely to change in the foreseeable future.

However, if we speak about the partner companies that have currently listed their loans on Viventor, there are a couple of things worth noting. The companies consist of professionals, possessing years of experience in non-bank lending and underwriting, and having their skin completely in the game. Also, access to financing for eligible borrowers is considerably faster than that offered by alternative creditors. This has been achieved by combining years of experience and knowledge with machine learning and other modern technologies.

What ROI can investors expect?

Currently, investors can earn up to 7% p.a. fixed, and there are no fees withheld. The number will be going up though, as we will be adding other types of loans with higher levels of interest.

Prestamos Prima, the mother company of Viventor, operates in Spain? What led to the decision to incorporate Viventor SIA in Latvia?

We as professionals have been in the non-bank lending for many years, involved in other projects before Prestamos Prima. While Spain is one of the major markets at the moment, it is certainly not the only one, and you can expect loans from other European countries being added.

What concerns Viventor being incorporated in Latvia – we are Latvians, and prefer to stick to our origins whenever we are able to choose. There is a lot of untapped potential and hidden talent in the Baltics, but then again – I believe people familiar with the European peer-to-peer financing market are well aware of that already.

Is the technical platform self-developed?

Yes, Viventor has been built in-house from the very first line of code, and we will keep the development of platform to ourselves. All in all, we believe the right approach for improving Viventor is by gathering feedback, applying our lessons learnt, constantly pivoting and optimising. And it is clearly much more efficient to achieve this with a dedicated engineering team in-house. Continue reading →