Just before the weekend Bondora sent me an email with a personalized investment overview video (click here to see mine; I was not able to embed it directly here in the blog). The video page encourages sharing via social media (Google, Linkedin, Facebook, Twitter), so obviously an aim is to aid in investor marketing. In future I might need to spend less effort on my personal portfolio reviews and post the video instead (just kidding). The highlighted return figure is higher than my own calculations, but I did achieve a high return on Bondora over the past years.

Have you seen other attempts on viral marketing via investors by p2p lending marketplaces? Let me know in the comments, please.

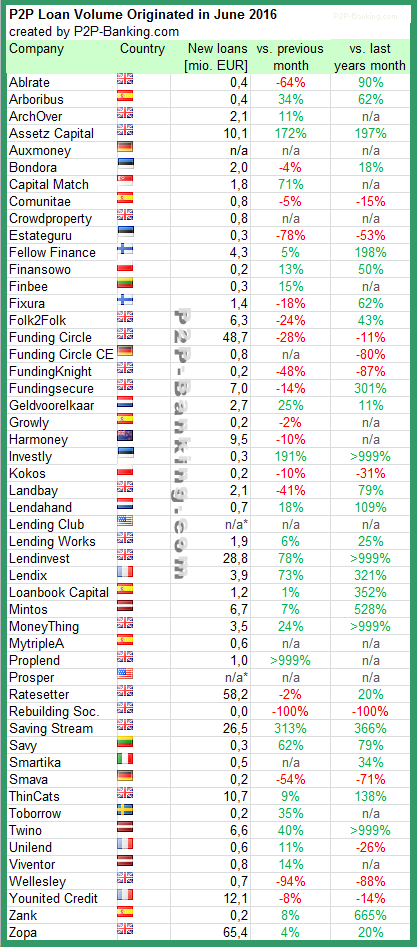

The following table lists the loan originations of p2p lending platforms in June. Zopa leads ahead of Ratesetter and Funding Circle. This month I added MytripleA. The total volume for the reported marketplaces adds up to 334 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in June 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

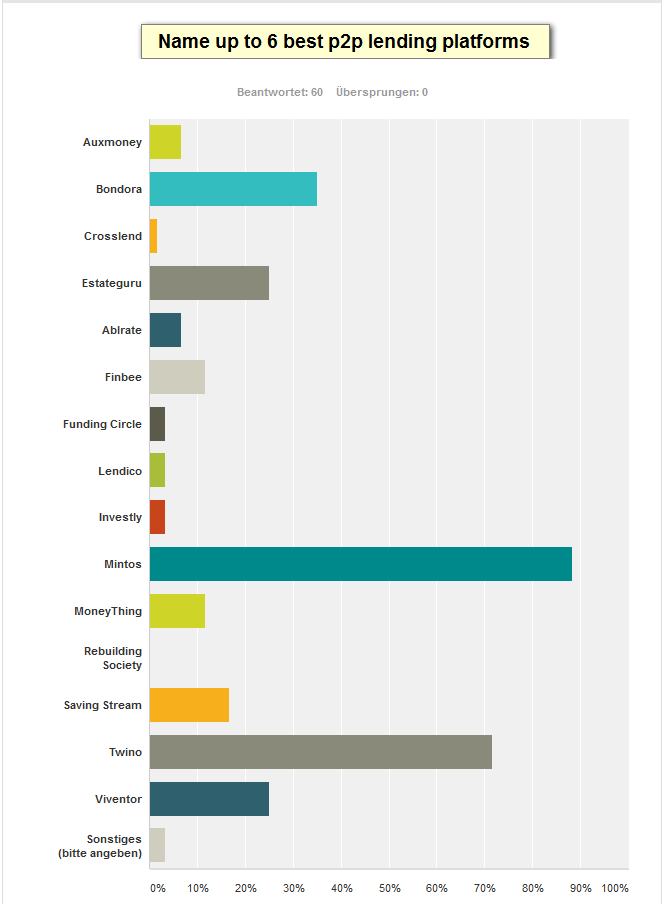

A poll conducted by P2P-Kredite.com among seasoned German speaking investors found, that many prefer p2p lending platforms outside the country they live in. After getting accustomed to the p2p lending concept and liking it, they are on a hunt for higher yields. Further supporting factors are the offered English language interface (a language most understand well), the easy transfer of funds within the Eurozone by SEPA payments and more features offered, e.g. most foreign platforms offer a secondary market, while currently none of the German marketplaces do.

Poll by P2P-Kredite.com, conducted in June 2016. 60 respondents. Each respondent could name up to 6 platforms. Note that Funding Circle refers to the German platform of Funding Circle, not Funding Circle UK.

Mintos (53 votes) and Twino (43 votes) lead by a wide margin in preference of the respondents, followed then by Bondora (21), Estateguru (15), Viventor (15), Saving Stream (10), Moneything (7) and Finbee (7). Exclusively baltic and british platforms rank best among the respondents. The choice of british platforms for German investors is limited though as some like Zopa or Ratesetter are open only to UK residents or require a UK bank account to sign up. Nearly all votes were cast before the Brexit decision. It remains to be seen how the UK platforms will rank in German investor preference in the future, given the more volatile GBP/EUR rates and the increased uncertainty for the UK economy.

The following table lists the loan originations of p2p lending marketplaces in May. Funding Circle leads ahead of Zopa and Ratesetter. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Table: P2P Lending Volumes in May 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

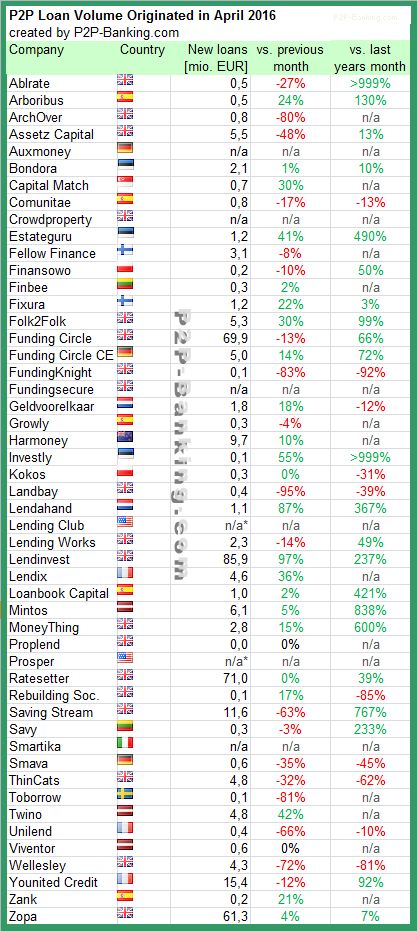

The following table lists the loan originations of p2p lending marketplaces in April. Lendinvest leads ahead of Ratesetter and Funding Circle UK. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Last month Younited Credit (formerly Prêt d’Union) originated first loans in Italy. Geoffroy Guigou told P2P-Banking.com, Younited Credit had a great start, with 416,500 Euro loans originated.

Table: P2P Lending Volumes in April 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

In October 2012 I started to invest into p2p lending at Bondora. I periodically blog about my experiences – you can read my update from Dec. 2015 here. Over the total time I did deposit 14,000 Euro and withdrew 13,380 Euro. So as you see I cashed out an amount almost equal to the amounts I deposited. The good news is that I still own 705 loan parts with an outstanding principal of 10,362 Euro at an average interest rate of 23.74%. Of these 6,355 Euro are in current loans, 1,004 Euro in overdue loans and 3,003 Euro in 60+ days overdue loans. The reason that I still have such a large loan book despite cashing out nearly as much as I paid in, is that I reinvested nearly all interest and principal repayments from 2012 till 2015.

Bondora shows a net return of 24.6% for my portfolio. In my own calculations, using XIRR in Excel, assuming that 30% of my 60+days overdue and 15% of my overdue loans will not be recovered, my ROI calculations result in 17.0% return.

Let’s look how my remaining portfolio is distributed by several criteria

Chart 1: My portfolio by country

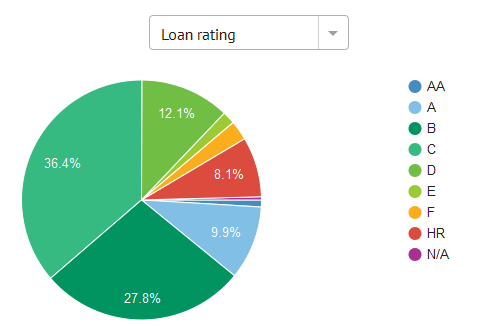

Chart 2: My portfolio by rating

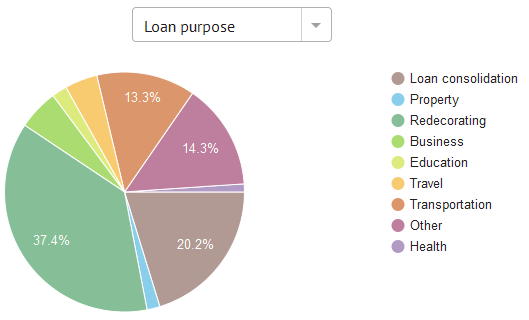

Chart 3: My portfolio by loan purpose

Recent developments

A lot has changed in the past four months. With the introduction of new regulation in Estonia, Bondora now prefunds all loans and also keeps a stake in the loans (‘skin in the game‘). Manual bidding on loans is not as straightforward as previously because now investors can make bids, which are not binding until allocation happens. This leads to situations were say 155% of the loan amount has been bid for, but the allocation has not happened yet, because some of the bidding investors have not enough cash in their account to match their bids and those bids that are sufficiently funded don’t add up to 100%. Furthermore Bondora gives bid preference to bids with larger amounts. If at allocation time bids with enough cash add up to more than 100%, then the bids for higher amounts will succeed, while the smaller amount bids will be rejected.