Invoice discounting marketplace Investly released a new version of the website today offering a redesigned investor interface. Investly allows investors to finance invoices sold by British and Estonian SMEs. Since the launch 11 months ago the number and volume of invoices financed has steadily increased. On the other hand rising investor demand pushed down the interest rates during the auctions to the minimum rate of 8% often during the past weeks.

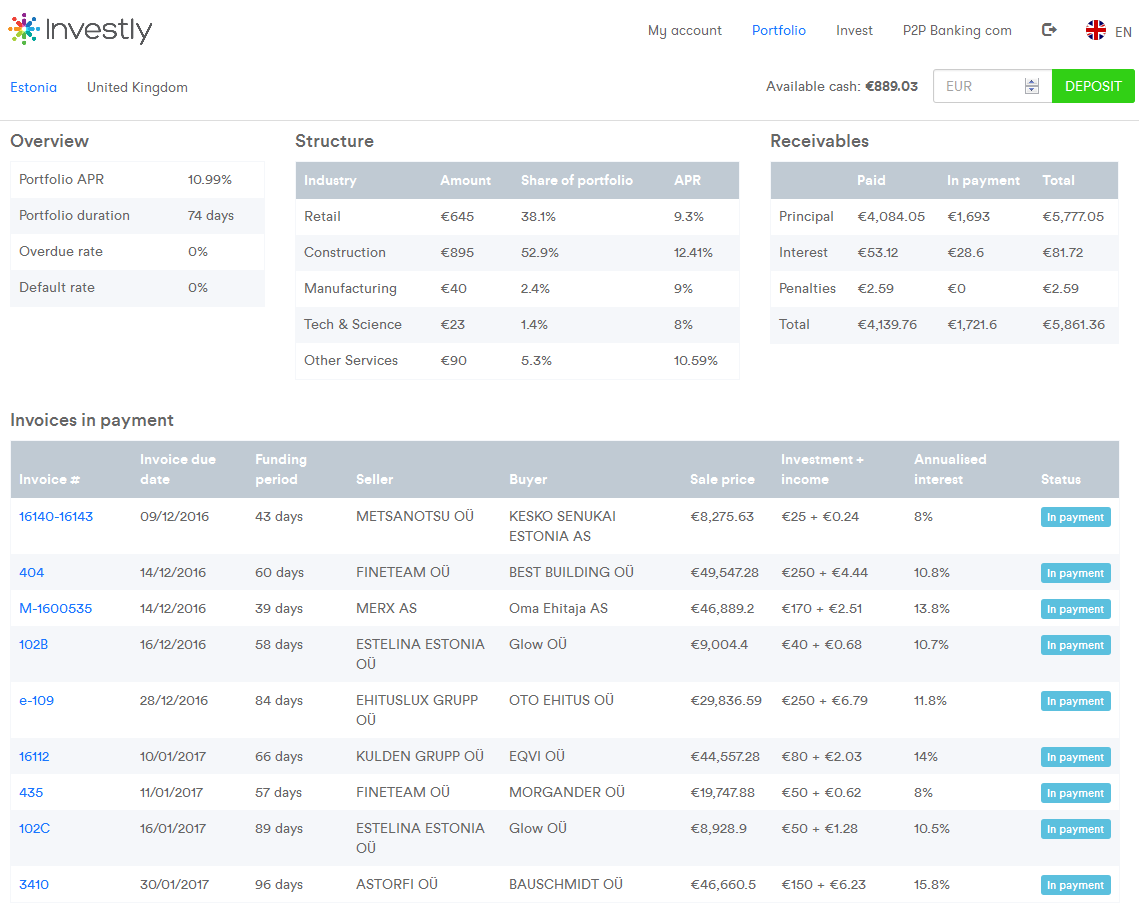

New Investly dashboard. View of my portfolio page. Click to enlarge

At the moment I don’t have any overdue payments – however in the past some payments were delayed for a few days. None of the invoices financed on Investly have defaulted so far.

Overall the new interface is a nice improvement and offers a better overview than the old layout. But there is still room for improvement. I would have liked it, if the tables were sortable for example. Continue reading →

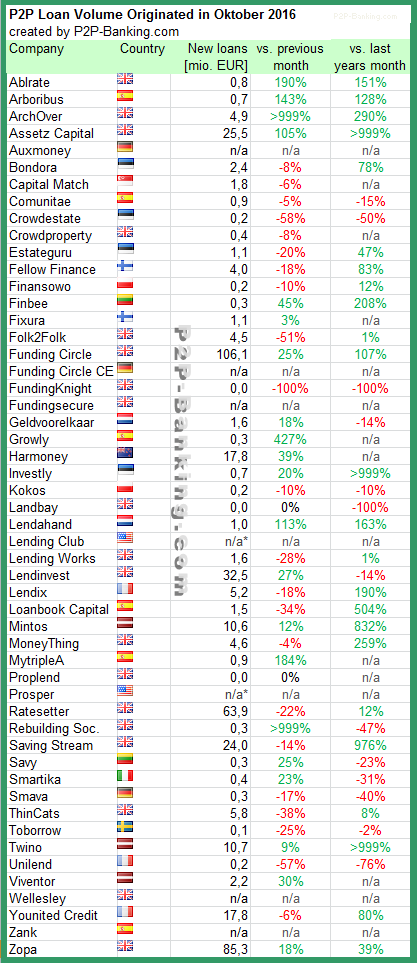

The following chart lists the loan originations of p2p lending marketplaces in October. Funding Circle had a record month ahead of Zopa and Ratesetter. Lendinvest has strong results too and Assetz Capital makes a big leap forward. The total volume for the reported marketplaces adds up to 443 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending platforms. Thincats crossed the 200M GBP funded this inception milestone.

Table: P2P Lending Volumes in October 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.

P2P lending marketplace Bondora announced that it will pull the primary marketplace from the user interface effective November 1st. This removes the chance for investors to manually invest on selected loans, leaving the options to either use the automated portfolio manager or to use the API.

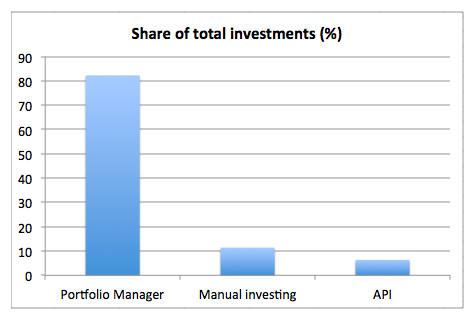

Earlier this week Bondora provided this statistic showing that the majority of investments is done through the portfolio manager. This is another of the many changes the Bondora marketplace underwent in the past years.

The announcement email sent today, reads:

On November 1, 2016 we will remove the Primary Market view from the user interface.

What does this mean?

In recent months it has become clear that the Portfolio Manager offers greater efficiency through automation compared to manually investing. The increasing benefits of Portfolio Manager are the result of recent updates to the funding process, which optimize speed. Moving forward we will continue to focus efforts on further improving Portfolio Manager, Bondora API, Secondary Market and the reporting features available on the platform.

Why is Bondora removing the Primary Market from the user interface?

Bondora is removing the Primary Market from the UI because the speed of our popular automated option meets the investing and borrowing needs before manual investing can take effect. Our process improvements have created an environment where almost all loans are funded before they become visible in the UI. As a result, the Primary Market is most of the time empty.

This scarcity is due to the fact that when a loan enters the market it is open to bids for 10 minutes. After the 10 minutes expire the loan is closed. Our internal analysis and reporting shows that almost 100% of loans are funded within this brief window of time. Therefore, there is little reason to hold loans open any longer, as doing so would create unnecessary delays.

What should API users do?

Removing the primary market from the user interface does not change anything for Bondora API users. However, API users should review their settings for polling loans from primary market and reconfigure their settings to match the changes to the current funding process. We recommend that the polling of new loans be set to once a minute. Our API allows for speeds up to one query per second, however such rapid polling is also not recommended.

Finbee is a small p2p lending marketplace for consumer loans in Lithuania (see earlier coverage). I have been using it as an investor for a little over a year now. My strategy on Finbee is different than on other marketplaces. I invest loans mainly with the purpose of trading in mind, that means on Finbee I don’t plan to hold the loan parts to maturity

Finbee secondary market basics

Loans can be offered at a discount, par or premium

Seller pays 1% fee upon successful transaction

Only loans with at least one repayment can be offered. This means I cannot sell loans directly after acquiring them on the primary market (no flipping). I have to hold each loan for at least 30 days.

Late loans and loans in arrears can be offered. Loans that are 60+ days overdue cannot be listed for sale.

Maximum listing duration is 20 days; thereafter seller can relist

Buyers can buy instantly at ‘buy now’ price or make a bid, hoping that no other buyer overbids them in the remaining listing duration (or pays buy now price)

Finbee parameter UI for selling loan parts on secondary market

How I select loans on the primary market

I mostly invest in ‘D’ loans (that is the most risky rating) with long loan durations (>36 months) and high interest rates. The average interest rate in my portfolio is 32%, the maximum 35%. My reasoning for this choice is that these loans allow high markups and still offer an attractive buyer yield (XIRR value). The longer the remaining loan term is, the lower will be the impact of the markup on the calculated yield for the buyer. I mostly buy 40 Euro loan parts, sometimes multiple in the same loan. I selected this amount because larger parts might not appeal to as many buyers, as some investors only invest small amounts.

Why I select different values for the reserve price and the buy now price

Since the XIRR that is displayed to the buyer depends solely on the buynow markup, it would seem logical to set same markup prices for the reserve price and the buy now price, doesn’t it. If in the example above I would set the price to 8.4% for both than I would get 8.4% markup if the sale takes place. With 8% and 8.4% values, I most likely get only 8% (at these markups there are very rarely multiple bidders competing). So why would I forego 0.4% gain? The reason is simple. With buynow the sale takes place instantly. But if I get the buyer to make a bid, the transaction takes place at the end of the listing duration, and all interest accrued during this duration is mine. Note that the buyer can NOT back out. He is commited and the sale will take place if he made a bid. In the above case the 20 days on a 39 Euro loan part at 32% mean I earn an extra 0,68 Euro (39€*32%/365 days*20 days) interest. So in effect if someone bid 8% on this loan my gain is 8%+1.74% accrued interest = 9.74% gain (which is much better than the 8.4% buy now). Of course I have to deduct the 1% seller fee.

BTW, I wondered how Finbee manages the sales with the accrued interest. When the buyer makes the bid, as said he cannot back out. But it is not clear if he will win (another buyer could overbid him) or how much interest will accrue for I as the seller have the right to accept the bid anytime early (which would only make sense if my cash is zero and I urgently want to bid on a new loan with a much better interest rate). But Finbee can’t wait until the time of sale because at that time, there could possibly be not sufficient cash in the buyer’s account. I couldn’t figure it out, therefore I asked Finbee. The answer is Finbee reserves the maximum possible price (principal+premium+maximum possible accrued interest) at time of the bid in the buyer account. Once the sale takes place, if the actual accrued interest is lower than the reserved maximum accrued interest, part of the amount is freed up. Continue reading →

The following chart lists the loan originations of p2p lending marketplaces in September. This month I added Crowdestate. Funding Circle, Ratesetter and Zopa had a record month. The total volume for the reported marketplaces adds up to 424 million Euro. I track the development of p2p lending volumes for many countries. Since I already have most of the data on file I can publish statistics on the monthly loan originations for selected p2p lending services. Milestones in total volume originated since inception:

Table: P2P Lending Volumes in September 2016. Source: own research Note that volumes have been converted from local currency to Euro for the sake of comparison. Some figures are estimates/approximations. The Wellesley volume is 0 for this month – this may be a reporting error. *Prosper and Lending Club no longer publish origination data for the most recent month.

BLender, a p2p lending company from Israel, today announced its global expansion, beginning with new offices in Milan, Italy and Vilnius, Lithuania that will serve customers in Italy and the Baltics. The Israeli-based company delivers a P2P lending platform with a proprietary consumer credit rating system designed for territories without credit bureaus or traditional consumer credit information. BLender is a cloud-based platform that was built to work in a wide range of markets and languages.

In Italy the platform charges borrowers a 4.5% origination fee and investors 1.5% of each repayment (principal and repayment). Compared to other marketplaces these fees are in the higher price range. The fee for selling a loan on the secondary market is 0.45%.

BLender has experienced exponential growth since its launch in 2014 and has already provided approximately 12 million USD in loans. The company will continue expanding its global operations into territories that are craving consumer credit. In 2017, BLender plans to launch operations in Africa, Latin America and other European Union (EU) countries.

“Offering multi-national P2P lending has been our vision since BLender’s establishment,†said Dr. Gal Aviv, CEO, BLender. “Since our Israeli launch in 2014, we have built the foundation, infrastructure and technology to enable BLender to operate in the global market, so we will be able to face operating, cultural, technological, regulatory and taxation challenges.â€

With the expansion into Italy and the Baltics, BLender is enabling users to lend and/or borrow across countries, making financial borders a thing of a the past, says the service.

“BLender identified a credit gap in countries where the supply of consumer credit is insufficient for the populations’ needs and is priced very high, and a gap in other countries where the savings options have very low or even negative yield,†said David Blumberg, founder and managing partner, Blumberg Capital, a San Francisco-based venture capital firm that led BLender’s last funding round. “BLender’s multi-national lending options mediate this credit gap by creating a meeting ground between borrowers from countries that lack consumer credit, to lenders from countries where the yield on their savings in insufficient. We support and strongly believe in the vision, management capabilities and business potential of the BLender team.â€

Investors on the BLender platform will earn predicted interest rates of 5-6% annually. The safeguard fund acts as an additional layer of protection to the lenders in case of a default. BLender’s default rate is approximately 1% before activating the safeguard fund. Thanks to the SafeGuard fund, the effective default rate is 0% says the service. BLender also offers ReBlendTM, BLender’s secondary market that offers the lenders the option the trade their loan portfolios and enjoy liquidity.

Recently BLender was chosen to participate in the exclusive ELITE program of the UK Stock Exchange that finds and nurtures companies with the potential for an IPO. As part of the program, BLender receives the guidance of the program’s experts for two years that help promote the company’s activity.

Furthermore, the company was selected as one of the most promising Fin-Tech companies in the world for 2015 by the accounting firm – KPMG, and also by the United Kingdom Trade and Investment Department.

The multi-national expansion was done in collaboration with KPMG.