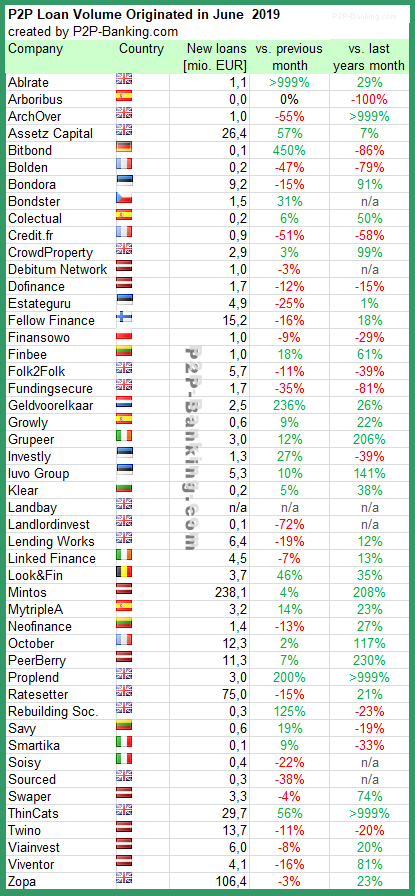

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 634 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones in culumulative volume lent crossed this month:

Table: P2P Lending Volumes in August 2019. Source: own research *The Mintos figure is a bit too low this month, as it misses the originations from the last two days.

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations.

This week some investors on the p2p lending marketplaces Viventor*, Grupeer* and Mintos* are affected by issues that hinder the normal procedures on these marketplaces.

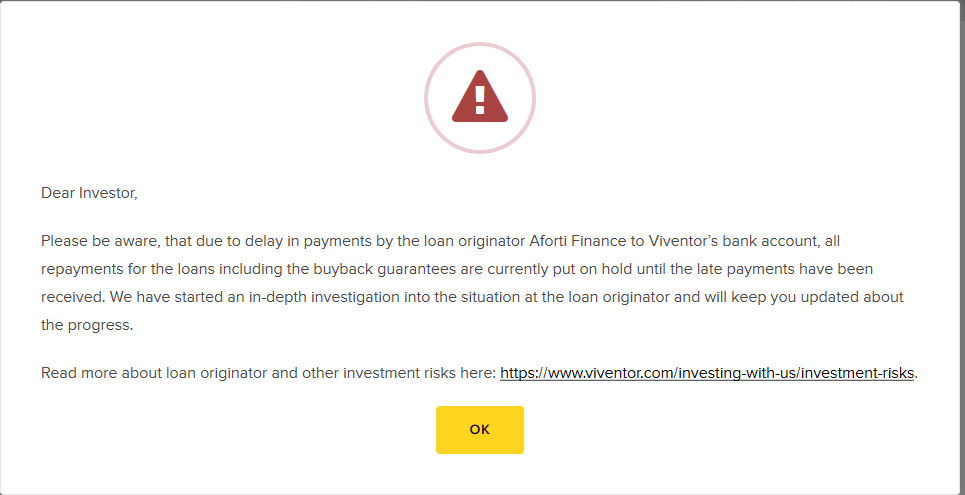

Viventor started to display the following warning message yesterday (visible only if you click on an affected loan)

(Screenshot from Viventor.com)

As a result, multiple Aforti loans were on offer on the secondary market for 5 to 15% discount (at one point in time I saw 35% discount)

Asked for a comment, Viventor CEO Andrius Bolsaitis told P2P-Banking.com:

According to information that we have now, they have some cash management issues, we are in discussions with them and hope to resolve the situation soon. I will be personally meeting with their managers tomorrow in Warsaw and will have more updates then.

Update 14:02: Apparently Mintos has now suspended trading of Aforti loans on the secondary market. I reached out this morning to Mintos’ management for a comment on how they see the situation with Aforti.

Update 14:42: Reply from Mintos CEO:

Hi … ,

Thank you for your email.Aforti is overdue on passing to Mintos payments which Aforti has received from borrowers and payment for buybacks. Thus, we are suspending repayments and buybacks. We are meeting Aforti tomorrow in Warsaw and will update investors accordingly. Below excerpt from communication to all investors: Mintos has suspended automatic repayments and buybacks for loans originated by Aforti Finance on our marketplace (EUR and PLN). The decision was made based on Aforti Finance’s overdue transfers of borrower’s payments to the Mintos marketplace.

In order to protect the interests of our investors, all loans issued by Aforti Finance have been removed from the primary and secondary markets of the Mintos marketplace. This means you cannot buy or sell Aforti Finance loans, effective immediately until further notice.

Update 16:02: Statement from Aforti Holding:

Dear Sir,

In response to the questions regarding the message released by Viventor, we would like to inform you following.

We are currently at the stage of closing cooperation with the Viventor platform, what has been announced to Viventor. Situation suggested by Viventor is a result of change in Aforti Finance S.A business strategy. Our decision is determined by technical difficulties in cooperation with Viventor platform. Also cause most workload has to be done manually, our operational risk increased significantly. This is what we want to avoid, cause AFORTI business model and operational procedures are going rather in the direction of using API to automatize processes and to minimize human errors.

It’s also worth to add, that we have not been using Viventor platform for new loans for about two last months, as a result of mentioned above decision. Of course Viventor receives daily financial transfers, so we do not see any reason for such a message.

Due to the fact that for tomorrow (Thursday, August the 8th ) we have scheduled a meeting with the Viventor, we believe all misunderstandings will be clarified.

Update Aug. 8th: the meetings are at 12:00/13:00 (Warsaw time)

Update Aug. 8th:Debitum Network*says investors on the Debitum platform are not affected as all Aforti loans were bought back on July 25th

As previously announced the meeting with Aforti took place in Warsaw. The parties found a solution with regard to the technical issues. We consider the solution satisfactory for both sides and expect all issues to be resolved during next week.

Update Aug. 12th: Mintos now says they had an agreement with Aforti since January 2019, due to which Aforti would not place any new loans on the primary market. Strangely they only communicate that agreement now. Why not in January?

Our team is once again meeting with Aforti Finance in Warsaw, Poland today to continue to work out the details of last week’s initiated solution for Aforti Finance to resume transferring borrower repayments to us for distribution among investors.

We aim to release the next more detailed update tomorrow.

Until then we thank you for your patience, as well as the questions to our Investors Service team and comments on the blog and social media. We are preparing to release answers to them as soon as we handle the current priority of resuming payments.

We also wish to remind that Aforti Finance has not been placing loans on the Mintos primary market since January 2019. It was a mutual agreement with Aforti Finance following a weaker than expected loan performance and IT system related issues. Aforti Finance has continued servicing the loans since then and the total Aforti outstanding loan portfolio on the Mintos marketplace has decreased from EUR 5.7 million on December 31, 2018 to current EUR 2.2 million as of August 12, 2019. In light of adverse changes in the mood on the Polish securitization and bond market as well as our due diligence insights on the company’s internal arrangements changes, we reflected our risk precautions by downgrading Aforti to C+ in March 2019.

At this stage we remain committed to working with Aforti Finance to continue servicing loans and passing borrower repayments to investors on the Mintos marketplace as soon as possible.

Update Aug. 14th: Mintos has announced that Aforti payments have resumed as of today. Aforti loans on the secondary market stay suspended.

Update Nov. 6th: Viventor has issued the following update:

… an update on the situation with the investments into loans issued by Aforti Factor S.A. and Aforti Finance S.A. on ViVentor platform, we want to update you on our actions regarding the repayment of loans, including the buyback guarantees, which were put on hold from the 6th of August 2019. On August 12th, 2019 ViVentor has negotiated and signed Settlement Agreements with Aforti Factor S.A and Aforti Finance S.A. Each agreement contained a daily payment schedule which was designed to ease up the cash flows of the companies and make it easier for them to repay their outstanding debt at that time. Both agreements expired on September 13th, 2019. By then Aforti Factor S.A has managed to pay all of their outstanding debt and the debt of Aforti Finance S.A. has settled their debt from the schedule on November 5th, 2019. However, new debt has been growing for both companies ever since and now we are taking all necessary actions, including legal ones to have the full amount paid of current and late dues and to protect the interests of our investors. … What is next? Our team is planning once again to meet with the management of Aforti Finance S.A. and Aforti Factor S.A. to continue to work out the details and find solutions to resume transferring borrower repayments to us for distribution among investors. The meeting date and place are being settled right now. We aim to release the next, more detailed update on our cooperation and ongoing payments executions within a few days (after the meeting has taken place). We would like to assure you that your concerns are of the utmost importance to us.

Earlier this week on Monday, it became evident that the Lithuanian central bank had suspended the operations of Satchelpay (source), which Grupeer* used as one of two ways for deposits by investors. From Tuesday onwards Grupeer asked investors to use the alternate deposit method via Baltic international bank only and said that they will add new payment providers this week.

Asked by P2P-Banking what the status of investor payments is, that were made shortly before or on the day of suspension to Satchelpay, a Grupeer contact told P2P-Banking:

At the moment we are in contact with the bank and have received the information that all transferred funds will be returned to the account of the sender. However, we cannot provide you with the exact terms. More detailed information will follow.

Hopefully both incidents will be resolved satisfactorily for investors. On both issues I see room for improvement on communications with investors.

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 611 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 613 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones achieved this month (total volume since launch):

Archover crossed 100M GBP

Credit.fr crossed 50M EUR

Arboribus is listed for the last time, as the platform will cease to originate new loans.

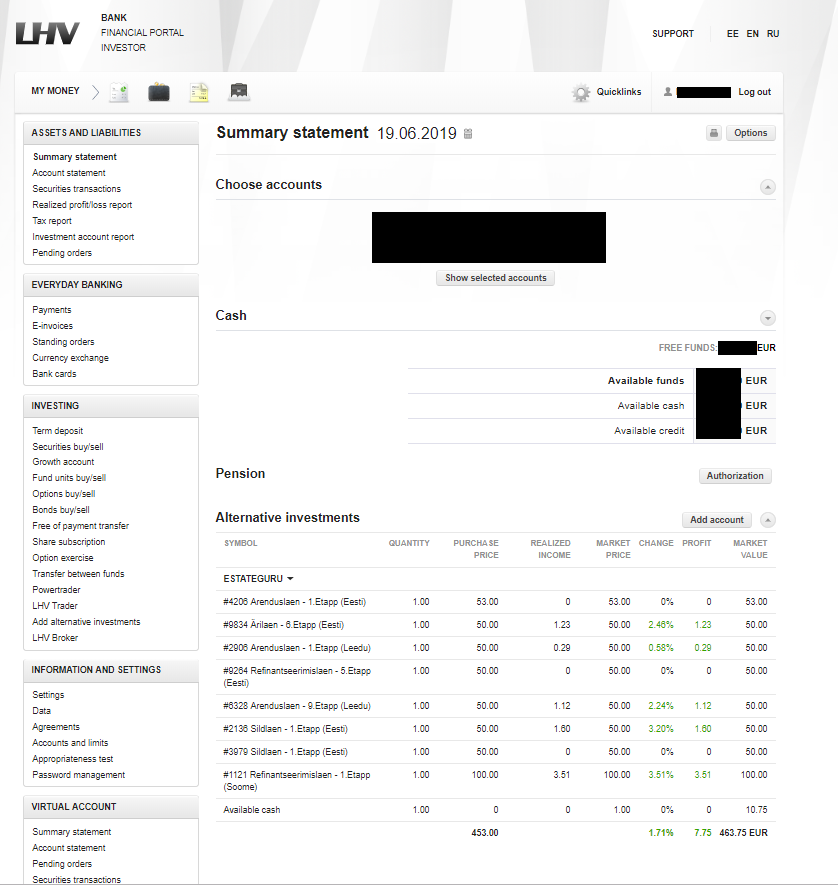

Who? What? You might wonder why that is relevant as most readers are unlikely to be LHV Bank customers. LHV Bank is a bank in Estonia.

I think it is highly interesting, as it is – to my knowledge – the first time a bank has integrated p2p lending investments in its customer interface. So the LHV bank customers, not only see their accounts and stock depots, but also their Estateguru* investments conveniently listed in their online bank dashboard. Much has been talked about what role could banks have in p2p lending (mere transaction banks? providing credit lines?) and also there is a lot of speculation if PSD2 (open banking) will help fintechs to seize the access to the customer from banks because they could control the user interface in the future. But this is actually a first step a bank takes in the opposite direction. By aggregating “non-bank” information inside the dashboard, they aim to make the banking interface more useful for the customers.

(Source: Estateguru)

Press release:

LHV customers can now see their short term property loan investments on LHV internet bank. On the summary view of internet bank, besides public stock exchange investments, one can see also alternative investments like short term property loan investments and cryptocurrencies, thus making it possible to get a quick and comprehensive overview of one’s investment portfolio. EstateGuru and Coinbase are the very first services to be switched on to the platform.

“LHV’s new service is the best example of cooperation between banks and fintech. LHV is most definitely a trendsetter in the banking sector. It is fulfilling to see that short term property lending has become a solid part of investments, and traditional banking has accepted it. EstateGuru has more than 25 000 investors throughout Europe, and the number is rapidly growing among both retail, professional, and institutional investors. We can provide our customers with more added value via interfaces like that of LHV’s “, commented EstateGuru’s COO Mihkel Stamm.

Alternative investments have become a substantial part of the Estonian investment scene, particularly among new investors. There are more than 13 000 people in Estonia who have invested in crowdfunding platforms. The fixed rate of return on debt instruments and access to the new and attractive asset classes have found their well-deserved place in investors’ portfolios. The better the quality of information, the more successful the investors.

“LHV aims to keep pace with its customers’ investment activities and that’s why we decided to take a step closer to the universe of alternative investments. The added value of this new service for our customer is a better and more comprehensive overview of the assets, thus making the portfolio management more successful “, added the Head of Investment Services at LHV, Martin Mets.

About EstateGuru

EstateGuru is the leading European platform connecting an international community of investors and businesses offering the highest diversification options for investors and flexible terms and speed of funding for businesses. The mission of EstateGuru is to provide hassle-free and flexible financing to property developers and entrepreneurs as well as diversified property backed cross-border investment opportunities to its international investor base—from the small individual investors to the institutions and everyone in-between. EstateGuru has more than 25 000 investors from 45 countries and the total money lent to date is more than 122MEUR. …

About LHV

LHV is the largest domestic financial group in Estonia. LHV’s mission is to help to create Estonian capital. According to LHV’s vision, the people and enterprises of Estonia dare to think big, start things and invest in the future. LHV’s values are to be simple, supportive and effective.

On Friday and Saturday I attended the P2P Conference* in Riga. It was the first p2p lending conference in Riga and I was very impressed how well organized it was for a new event. Kudos to the Targetcircle staff who organized that. The audience was platforms, retail investors and bloggers/youtubers mainly from the Baltics and Germany but also sprinkled in from other countries all over Europe. I would estimate about 350 to 400 people in total.

Platforms presenting and attending were nearly exclusively from Eastern Europe (mainly the Baltics). Most of the retail investors came for the chance to meet and speak to the platform representatives in person.

The organizer of the conference is Norwegian affiliate technology company Targetcircle. Targetcircle was founded in 2014. I became aware of them when Mintos switched their affiliate tracking from an inhouse solution to their system around November 2016. Since then they won a wide variety of Eastern European p2p lending platforms as clients for the affiliate tracking solution, but also recently the Irish platform Flender*. Targetcircle concentrates on the underlying technology as a marketing solution for fintechs but also as a (whitelabel) technology for other affiliate networks. The CEO told me he aims next to win more clients for his solutions in the UK and Spanish market and then later on in East Asia.

The conference started with a day of presentation, demos and time to visit the exhibiting platforms at their booth. There was ample time for networking with good catering (outside barbecue with DJ music). A recorded livestream video of the main stage activity is available here.

I really enjoyed the opportunity to talk to so many platform representatives, other bloggers and hear the opinion of many retail investors from recently started to 10+ years investing into peer to peer lending. In general the investor crowd was optimitic about the future prospects of investing into p2p lending and we all exchanged experiences, opinions and tipps on strategies, selecting platforms and evaluating risks.

The atmosphere was very relaxed and informal and it moved to a vacation feeling when on Saturday the venue was located on a beach at a lake.

Attendees spent most of the time chatting and networking, but some more venturous ones took up the offer to try wakeboarding or stand up paddling or got active playing volleyball or boule.

Targetcircle plans to do the conference again next year and I am looking forward to going again.