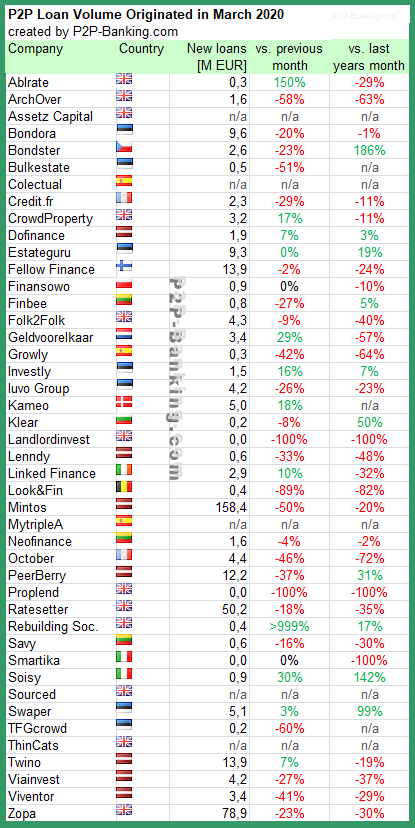

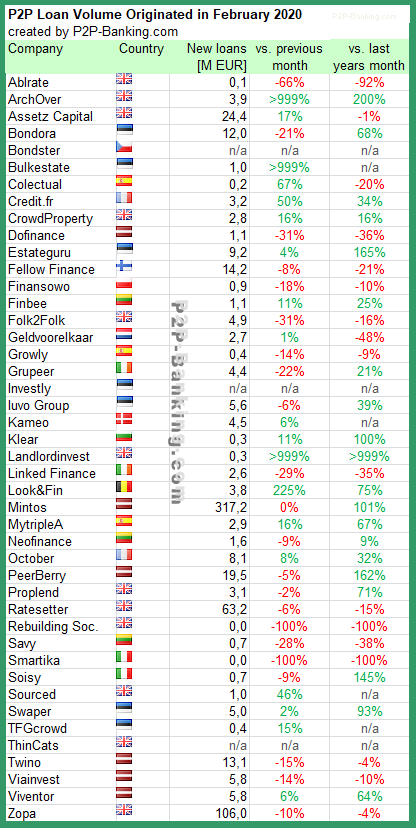

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 397 million Euro, down 40% to the previous month. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Lenndy*.

Milestones achieved:

Mintos* crossed 5 billion EUR originated loan volume since inception

The effect of the current crisis is impacting nearly all marketplaces significantly in the second half of March. Read my previous article ‘Hunger for Liquidity – State of P2P Lending in Times of the Coronavirus‘ for further observations on this. To counter the effect the sinking volumes has on revenues of the marketplace company, Mintos* and Assetz Capital* announced the introduction of new fees for investors.

Not only the stock markets, but also the p2p lending sector is heavily impacted by the current coronavirus situation. In this article I’ll try to give an overview of what’s currently the situation.

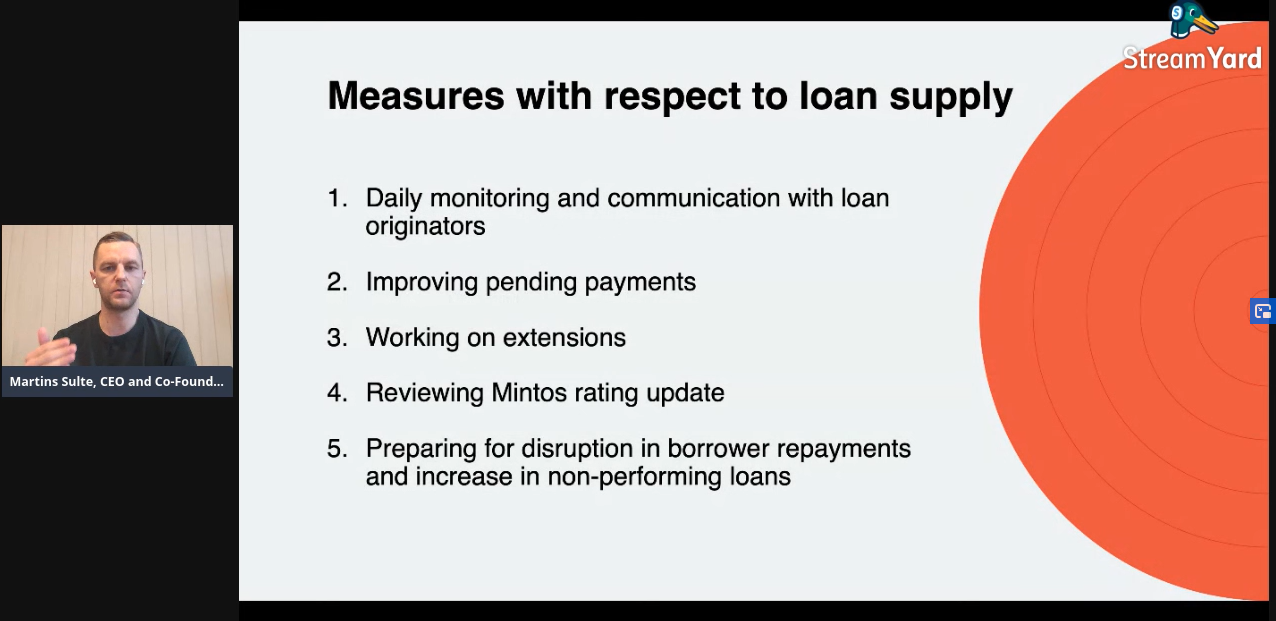

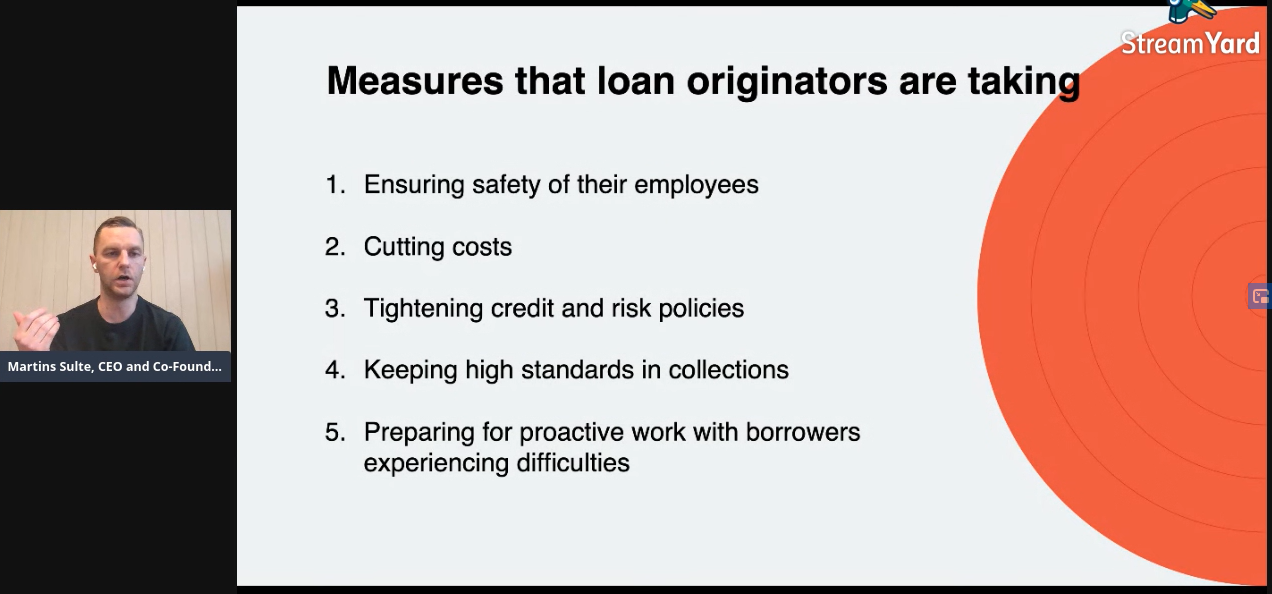

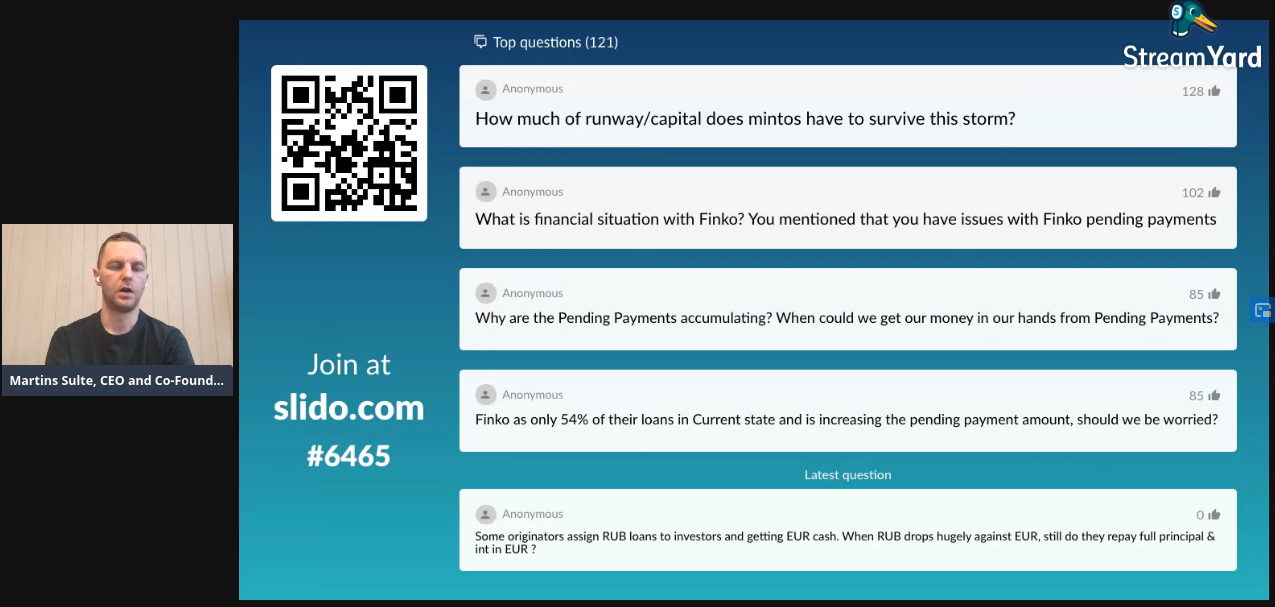

I watched the Mintos* live webinar on the current situation for the past 90 minutes. Some screenshots of the slides shown are at the end of this post. About 800-900 Mintos investors were watching and I think they highly appreciated the time and effort Mintos took to communicate. CEO Martins Sulte spent over 45 minutes answering questions. And there are a lot of questions investors have in times like these.

My take is, that the biggest trend we saw in p2p lending in the past week is the hunger for liquidity. Both on the investor side as on the loan originator side (on those marketplaces that work with loan originators).

105 German investors participated in a poll I ran over the past two days. Of these

11% say they increase their p2p lending investment, to buy and profit from loans that are available at (large) discounts on secondary markets

3% say they are increasing their p2p lending investment for other reasons

30% reinvest as usual

26% are withdrawing money as the want to reallocate it to the stock money

20% are withdrawing money as they think the risk is too high

So even in this small, non-representative poll nearly half the investors are saying they are withdrawing money.

How that impacts the p2p lending marketplaces can be observed exemplarily on Mintos* :

loans on offer rose and still rise sharply both on the primary market (900,000 loans) and on the secondary market (1.7 million loans)

as many investors scramble to exit, this is only possible for them if they offer extreme discounts on the secondary market (the highest discount for current loans on offer is currently -20.1%, resulting in YTMs of 30% and higher for the buyer)

The volume of newly financed loans on the primary market has tanked

Interest rates offered on the primary market rise (current maximum 21.1%, Mintos even had to adapt the range the slider in the UI could show), together with cashbacks on offer and there are also measures to tie in capital longer.

In the current situation most investors in the discussion seem to assume that elevated risks come by the potential inability of borrowers to repay the loans, due to economic downturn. That may well be, but would impact the yield mid- or long-term (weeks or months). In my view there are two very short-term risks that many investors overlook:

The currency risks for many Mintos loan originators: Many have issued loans to borrowers in weak currencies like RUB, KZT or GEL, but need to pay Mintos investors in EUR. The sharp change in exchange rates could pose major problems for the liquidity of the loan originators.

Many loan originators were growing fast and required constant cashflow to finance their lending and operations as they were not yet profitable. Some were even leveraged. External refinancing might be very hard to impossible to obtain in current market conditions (see for example investors reaction on trading of the Mogo Finance bond). And as said the volume financed on Mintos primary market is slowing. Again this could pose liquidity problems to originators.

An industry insider I spoke to said he would expect at least 2-3 loan originators to fail short term. CEO Sulte acknowledged in answering the questions on the webinar that “not all” could be expected to make it in the current situation, pointing to the large number of loan originators active on Mintos.

The two cited short term problems are especially a concern on those p2p lending market places that operate with loan originators. Of course the investors are also withdrawing increased amounts on “classic” p2p lending marketplaces like Assetz Capital, Bondora, Ratesetter and Zopa, but this poses no short-term risks to the stability of these marketplaces in my view.

Other investors share this opinion, pointing to the different levels of discounts on different secondary market (for current loans: Mintos* -20.1%, Viventor* -6%, Iuvo* -5.7%, Finbee* -5%, Savy* -5%, Neofinance* -5%, Bondora* -3%)

The platforms have reacted by four ways: communication, temporarily suspending borrower repayment requirement (especially SME loans, e.g. Linked Finance, October, Neofinance* ), and stepping up marketing and increasing interest rates:

Bondora* runs a raffle for investors which can win a BMW, minimum investment 1 EUR required.

Lendermarket* has increased interest rates from 12 to 14% and offers 2% cashback for any investment increase

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 660 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Bulkestate*.

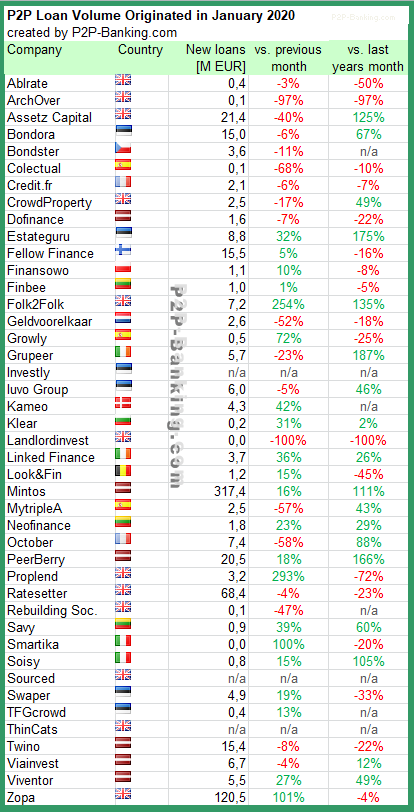

The table lists the loan originations of p2p lending marketplaces for last month. Mintos* leads ahead of Zopa and Ratesetter*. The total volume for the reported marketplaces in the table adds up to 690 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. I removed Boldyield as the platform has paused lending and repayed all investors (including accrued interest).

Milestones in cumulative volume lent crossed this month:

I am looking forward to attending the P2P Conference 2020*, which takes places in Riga on June 19th/20th. If you want to go too, you can order your tickets using this link P2P Conference 2020* together with code Claus for 20% discount (click on ‘enter promo code’ on the page where you enter the ticket quantity).

I went to the conference last year and enjoyed it. You can read my article about it here.

This year I plan to arrive a few days earlier (on the 16th) in Riga, using the time to meet up with platform representives. I also plan to organize a lunch or dinner meetup for P2P-Banking readers so we can chat and discuss current p2p lending developments. If you are interested send me an email and I’ll inform you once the planning is further advanced.

The website is down. Several investors voiced complaints on Facebook, Twitter and forums, about not receiving withdrawals within 5 working days, the time-span that the company used to tell investors is the normal processing time. Social media profiles of several management members were deleted today. The European Crowdfunding Network reported them to authorities after receiving multiple investor complaints.

The platform Envestio was launched in spring 2018 and promoted business loans of a wide variety of types (crypto, real estate, working capital, …). Founded by management with Latvian origins the platform was officially run by Envestio SI OÃœ, a company registered in Estonia. Business loans (not consumer loans!) are currently not subject to specific regulations in Estonia.

Initially most of the offered projects came with loan sizes of 100K EUR to 300K EUR, but recently offered projects got much bigger. Offered interest rates where high, often around 20%. Shortly after the start, Envestio started to offer a ‘buyback guarantee’ (later renamed ‘Repurchase Guarantee‘) under which it would repurchase loans prematurely for a fee of 5% should the user request it.

To date Envestio seems to have collected around 33M EUR of investor money from about 13,000 investors throughout Europe (number according to Envestio website before it went down). Analysing web traffic, which probably correlates to investments, I would estimate that most of the investors came from Italy, Denmark, Spain, Germany and Portugal.

All seemed to go well for Envestio. Certainly the investments looked extremly high risk. I never invested as it was way beyond my risk appetite, but nobody suspected a scam.

In summer 2019 the company announced it was sold to a new owner.

Then there were allegations from an anonymous Twitter account (@RPeerduck, meanwhile deleted), published on Dec. 18th 2019. These linked the new Envestio COO to fraudulent promotions for an investment scam years ago. I asked the Envestio management for comment and received an email explanation on Dec. 20th, 2019, in which the COO said ‘… At the same time, the only personal experience in this sphere that I have is making a presentation of crypto-project, management of which was able to prove that their company can be trusted and does not have any signs of scam at the moment of making this presentation.. ‘. I did not find the offered explanation convincing at all.

Combine that with a media article in the Latvian press where a team member of Envestio was accused of misconduct in a former job (she denied any responsibility or misconduct), that left me wondering if Envestio is complying with all legal obligations.

All these bits of information were discussed on various forums. Nevertheless many investors seemed undeterred. As late as yesterday many investors on Facebook were defending Envestio’s arguments. The last one was a DDOS attack by hackers that disrupted the service.

The last withdrawals payouts that users actually received according to investor postings, were requested on or before the morning of January, 12th.

The last statement Envestio published on its Facebook page yesterday reads ‘…Simultaneously with the recent concerns within the industry, we tracked repeatedly various technical attempts targeted to influence dramatically on stability of Envestio platform. They were performed through hacker attacks on our web site and platform’s internal structure and database.

At the same time, we noticed that destructive public relations campaign against Envestio has been initiated and which consisted of spreading knowingly false and unconfirmed information by numerous internet resources questioning financial stability and reliability of our platform, denigrating the reputation of the Envestio owners and key employees.

We tend to consider these attempts as a consistent and well-planned set of actions aimed to cause significant financial and reputational damage, as a result of which the Envestio platform should inevitably begin to experience substantial difficulties with current payments to its investors.

We assume that the ultimate goal of all these actions is to devalue overall Envestio’s business, and the subsequent potential raider takeover of the company or an attempt to eliminate the company from the industry, getting rid of as strong competitor. The implementation of the aforementioned scenario is evidenced by a number of factors and hostile actions that occurred precisely at the moment when a serious crisis of confidence reigned in the crowdfunding market and which actually was caused by the scandal surrounding the activities of the Kuetzal platform. …’

What options of actions do investors have?

Investors believing that they are victim of a fraud could complain to the authorities e.g. the Estonian police, email ppa@politsei.ee . Clearly state what you are complaining about, provide documents, state your identity. I reached out to the press department of the police today, but have not yet heard back from them.

Investors could also elect to have a lawyer represent their interests.

EDIT: 23.01.: One team member posted claiming innocence/not knowing what was going on (I have no means to verify if the post is really from the person with that name)

EDIT: 23.01., 14:50: Statement from a press officer of the Estonian police in response to the inquiry of P2P-Banking: : ‘In the past few days, the Estonian police have received several complaints regarding the crowdfunding platform Envestio. We are currently working to specify all details, but there is no investigation underway. However, if signs of crime do surface, we will start an investigation.Head of the Fraud and Economic Crime Division of North Prefecture Juhan Ojasoo: „Not every unsuccessful investment is fraud, however, if one really believes they have been deceived, we encourage to get in touch with us.“

A statement can also be submitted via e-mailing ppa@politsei.ee and describing the case in as much detail as possible. We ask to provide contact details, amount of money lost, dates for transacations etc.

We also advise checking the Estonian Financial Supervision and Resolution Authority website for alerts prior to investing in any company: https://fi.ee/en/alerts.’

EDIT 24.01., 14:59 There are serious concerns (source) too, regarding the Estonian platform Monethera. Monethera has claimed a relationship in the past with Richly Pacific International Ltd, from Hong Kong, register number 1543697. A search in the document register shows that this company was dissolved in December 2018 already. EDIT 24.01. 21.32: Monthera stated ‘It’s a mistake and we already contacted Hong Kong companies register’

EDIT: 24.01. 17:35 Further concerns surfaced about Wisefund, a company with a model that has similarities to Monethera. An investor claimed a borrower listed on Wisefund denies having asked for a loan . There is a statement that Wisefund gave to another investor as an explanation, which does not convince me personally. You can read about this here.

EDIT 24.01. 18:03: J. V. (name shortened) on FB has shown a direct connection between a team member on Monethera and Envestio. The team member owns 50% of the sponsor Baltic Real Estate Holding (Barona 72 sponsor) which was a project on Envestio.

EDIT: 29.01.: 15.23: Update by Estonia police to P2P-Banking.com:Â ‘This week Estonian police began a criminal investigation regarding Envestio. The case is being investigated as investment fraud.‘

Head of Economic Crime Bureau of Central Criminal Police Leho Laur told P2P-Banking: ‘We have received a large number of appeals from people who have invested into the crowdfunding platform Envestio. Majority of the appeals are from people outside of Estonia. We are currently working through the statements received and communicating with other Estonian investigative organisations, who have also received complaints regarding Envestio. We know that the number of people who have put their money into Envestio is even larger, thus, we are likely to receive more complaints.

Our first objective in the investigation is to find out wheter it was fraud and the platform was created with the purpose of deceiving people or the website was closed due to a bad investment. It is also important to identify the people connected to this company and determine, wheter the crime was committed in Estonia or elsewhere. This is an investigation that has many parties and we will be cooperating internationally as well.

The Economic Crime Bureau of Central Criminal Police is working to establish how money was moved between accounts. Usually, in international fraud, the money is quickly moved between accounts in different countries until it is withdrawn through an ATM. Due to this, the chance to recover the money is small.

Most active crowdfunding platforms are trustforthy, but we recommed to always check where you are placing your money.‘

State prosecutor Sigrid Nurm told P2P-Banking: ‘Before investing into a company, it is necessary to do some background work and check where exactly the money will be placed. A promise of a high return and claimed amount of people involved or money invested, should not be viewed as guarantees. We recommend to look past advertisements, social media posts and websites, and to look into the background of the company in more depth. Look into open source registries, consult with your home bank or a local Financial Market Supervision Authority. It is also important to remember that every investment carries a risk and losing money does not necessarily mean that it was fraud.

A statement can be submitted by e-mailing ppa@politsei.ee and describing the case in as much detail as possible. We ask to provide contact details, amount of money lost, dates for transacations, description of what happened etc.

Currently we have no reason to believe that the two platforms, Kuetzal and Envestio are connected.‘

EDIT 29.01., 21:48.: After looking at documents compiled by Envestio investors on Facebook regarding the status of individual loans I believe the potential damage caused by Envestio is closer to about 22 million EUR (plus uninvested cash lying in accounts) This is because at least 13.98 million EUR loans are in the status ‘repaid’ I assume that investors mostly reinvested (or withdrew) that money. While the 22 millions are lower than the 33 million EUR mentioned at the top of the article, it is still a huge amount.

EDIT: 31.01., 18:45: Estonian police publishes a ‘FAQ’.

EDIT: 02.02.: According to a press article, Latvian police have not opened an investigation but promises to support Estonian police if necessary

{kind=link}