Plenti*, formerly Ratesetter Australia, is seeking to raise 55M AUD from investors in Australia and New Zealand through an IPO. The IPO takes place from Sep. 7th and the plan is to list the shares on the Australian stock exchange on Sep. 23rd.

The Plenti IPO prospectus reveals that Plenti will be valued at 280M AUD in the IPO.

Plenti wants to use the majority of the raised capital for warehouse funding for equity tranches and as working capital (see section 7.1.2)

Plenti’s Chairmen Mary Ploughman states: ‘Plenti’s proprietary technology platform provides borrowers, investors and commercial partners with simple digital experiences. The Company believes its technology platform provides a meaningful competitive advantage in markets where speed and ease of services are increasingly important, and believes its technology platform provides an important foundation to support continued growth and operational leverage over coming years.’

The initiative comes after Ratesetter UK announced it will be acquired by Metro Bank. The shares Ratesetter UK held in Ratesetter Australia were not part of the operation and the 18 million shares Ratesetter UK held in Plenti (Ratesetter AUS) will still benefit the original shareholders in Ratesetter UK.

As of August 2020, Plenti has originated 724 million AUD (this figure is from the online statistics, the prospectus states 870M) in consumer loans since the launch of the marketplace in 2014. In July 2020 Plenti introduced maximum rate caps for investors forcing interest rates down in order to attract more borrowers after the new volumes had about halfed since the start of the COVID 19 crisis. Ratesetter results for the financial year 2020 (ending March 31st, 2020) were a loss of 16.4M AUD (see section 4.7).

less defaults: 0 AUD (as all loans are covered by the provision fund)

Unlike on other platforms, I did not stop my autoinvest at Ratesetter AUS when the crisis evolved. My main reasons were that the provision fund is quite reasonably filled (>10M AUD) and I did not want to change the funds back to EUR currently, so rather than withdrawing them and storing them in AUD cash without any interest I figured I could just continue to reinvest them.

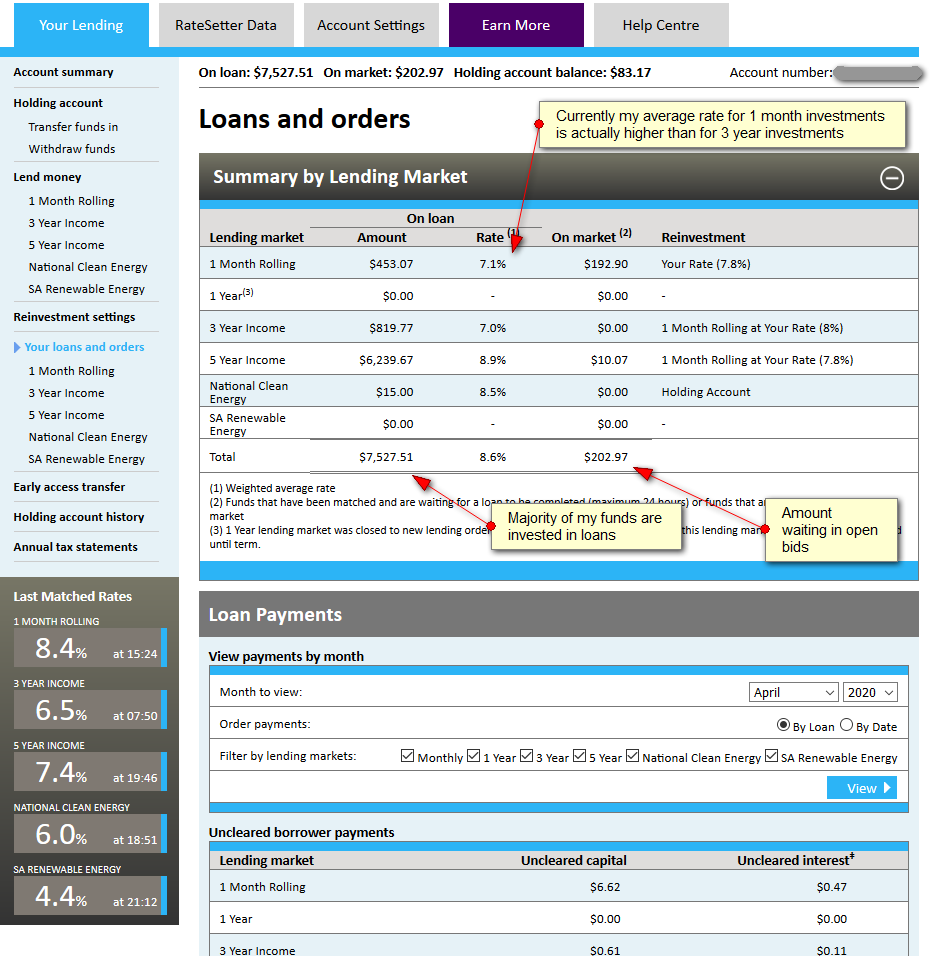

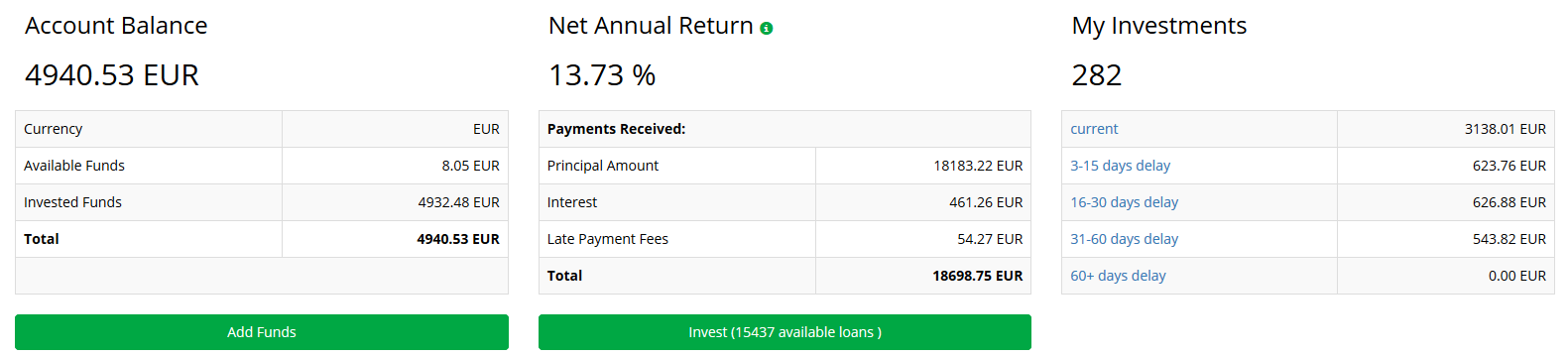

I now reinvest only at the 1 month market as the interest rate there is frequently peaking at higher rates than on the 3 or 5 years market. The following screenshot shows the current allocation of my funds at Ratesetter.

click on image to enlarge screenshot

What measures did Ratetter take in reaction to the pandemic effects on the market

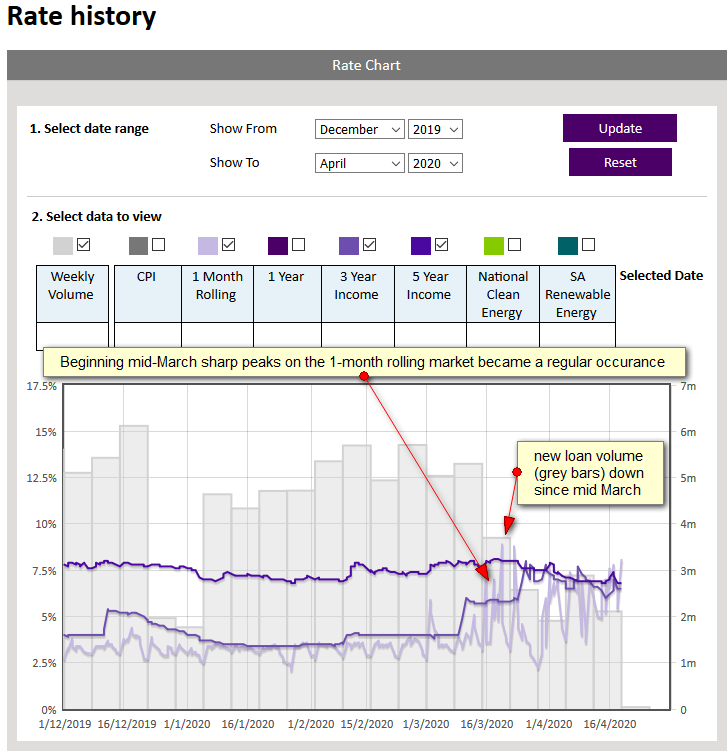

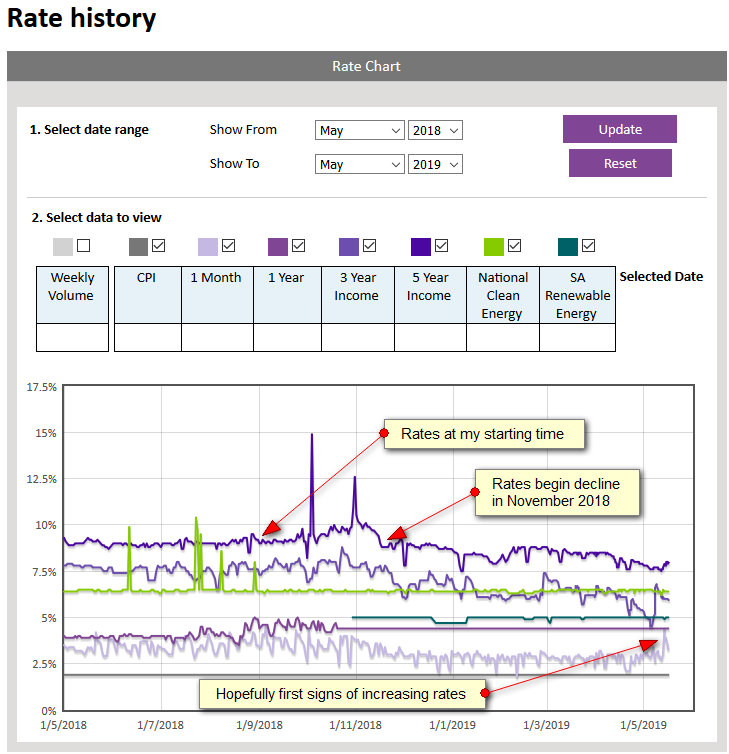

In early March market turmoil caused temporary spikes of interest rate matches up to 19.9%. This was mainly caused by less lender money than usual offered. Starting on March 23rd, Ratesetter imposed a maximum ceiling of 9.0% for the lending rates on all markets. Older bids that were higher were cancelled.

In the following days investors mostly reallocated remaining funds on offer away from the longer term markets to the 1 month market.

On (or about) March 25th, the remaining funds on the 1 month rolling market must have fallen below the funds replacement buffer of 300K AUD, invoking section 7.7. of the product disclosure section, meaning paybacks on 1 month loans are not return to investors but rather reinvested at the previous rate. While it happend a few time to me since then, it is not really a problem (even so it is relent at pre-crisis interest rates of 3.5%), as I had very little funds on the 1 month market.

The following chart shows the turbulence starting mid-March, with rates bouncing up and down since then.

Overall the main impact on Ratesetter so far is the drop in new loan volume and the much higher interest rates on the monthly market. As far as I can tell repayments on the loans arrive regulary and if there is an impact on default rates it still lies in the future.

click on image to enlarge screenshot

Another big fallout of the crisis has been the forex impact. My home currency is EUR. Compared to that currency, the Australian dollar abruptly devalued in March. I even considered excahnging additional Euro to gain of the exchnage rate drap, but decided against it. The rate has moved back in the direction of pre-crisis levels since. As I have not withdrawn any money from Ratesetter the exchange rate fluctuations have not impacted me.

I covered my p2p lending portfolio periodically over the past 12 years in this blog. The following report is a snapshot on how it is composed right now (May 2019) and which strategy I will take for the next months. As you can see below I aim for a widespread diversification (over different platforms as well as geographically) of my p2p lending investments.

Mintos

Mintos* is my biggest position. I run a trading strategy on Mintos. Mintos gives my net annual return as 15.1%. Calculating it myself based on the deposits and withdrawals I get a XIRR value of 24.8%. The cause for the huge discrepancy is that Mintos does not account correctly for the cashback of the campaigns. I heavily traded, when Mogo ran a campaign. For example I invested in new Mogo loans that were offered with a 2% cashback on the primary market, nearly instantly sold them with 1.8% discount on the secondary market and pocketed the cashback. Rinse and repeat.

I am satisfied with the current degree of diversification over loan originators in my Mintos portfolio. The bulk of my investments is in loan terms between 3 and 30 months at interest rates ranging from 13% to 15%. The lower interest rate loans are usually only held temporary as part of my trading strategy.

For the coming month I plan to keep my Mintos* investment at roughly that amount, reinvesting the paid principal and interest. New investors registering via this link at Mintos, get 1% cashback on amounts invested in the first 90 days. Mintos is currently not accepting UK investors.

Linked Finance

My second largest p2p investment is on Irish SME loan platform Linked Finance.

Diversification achieved is good. The majority of my loans have interest rates between 8% and 11%. Most loan terms are 2 or 3 years.

I “collected” 7 loans in default (double dip on the golf loan). But 5 of these had repaid more than half the principal before they want into the default state so the principal in default sums up to only 270 Euro. My self-calulated XIRR value is 6.4% if I totally write off the amounts in default and 7.1% if I assume that half the amount in default will be recovered. I plan to slightly increase my Linked Finance* portfolio in the next months. Linked Finance is not offering any cashback or bonus rewards for new investors.

Bondora

Bondora is my third largest and oldest (still running) p2p lending portfolio. I started in 2012. My self calculated XIRR value is 16.6%. A yield that high is not achievable nowadays anymore. My portfolio profited heavily from the first years when interest rates were typically 28% to 34%.

I am currently investing into Estonian A and B loans using these autoinvest settings. I have used these settings unchanged for 11 months now and it is running totally hands-off with no maintenance required.

On Bondora* I reinvest the bulk of my repayments and occasionaly withdraw some funds. New investors registering on Bondora using this link get a 5 Euro sign-up bonus.

Ratesetter Australia

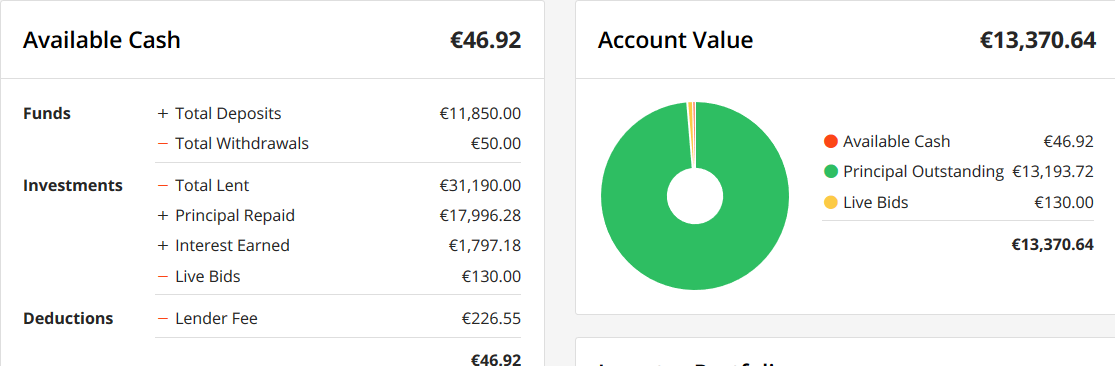

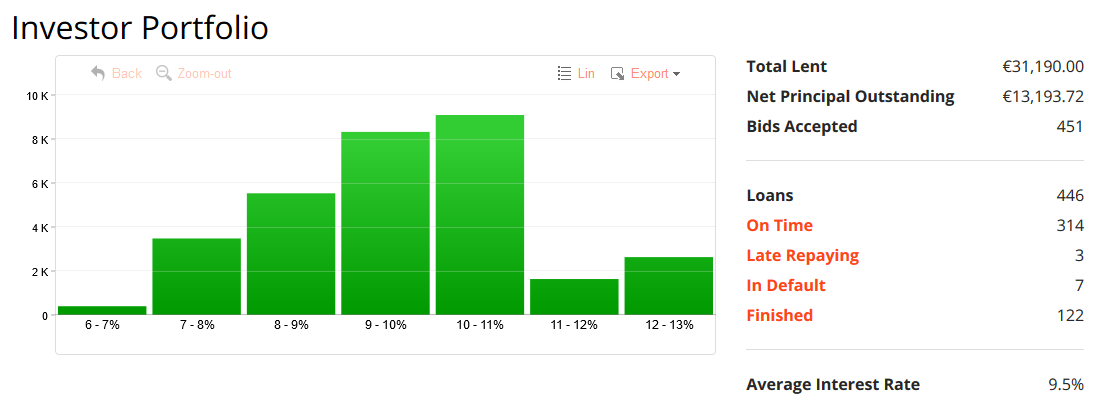

Ratesetter Australia* is my fourth largest p2p investment and also one of my youngest. I started in August 2018. My XIRR value self calculated in AUD is 9,1% if I include the 75 AUD sign-up bonus and 7.4% if I do not include that.

My money is mostly invested on the Ratesetter 5 year market at an average rate of 9.2% (that is after fees but before withholding tax).

In the past months the interest rates have dropped considerably therefore I am parking some funds on the 1 month market or invest them on the 3 year market.

I am reinvesting all repayments at Ratesetter Australia. If rates go up again I plan to do that on the 5 year market, otherwise I’ll settle for the 3 year market. It is a little complicated to register as a non-resident, but I have described how I managed to sign up as a European here. New investors can earn a 75 AUD promotion bonus by investing 2,000 AUD or more in our 3 year Income or 5 year Income lending markets before 31st May 2019. Achieving that requirement in time will not be easy, even if you start directly.

Iuvo Group

The fifth largest position of my p2p portfolio is invested at Iuvo. It is running hands-off and does not require any maintenance.

I continue to reinvest all repayments. Iuvo pays new investors a very generous cashback of up to 90 EUR. For more details and how to get it see the cashback overview page.

Estateguru

After I completely exited Lendy in last autumn, baltic Estateguru* is now my largest platform for property secured loans. I don’t use the autoinvest. Instead I periodically login and manually invest into a new Estonian loan secured by a first rank mortgage.

I mostly reinvest all repayments. New investors get 0.5% cashback for all investments in the first 90 days, if they sign up using this link.

Fellow Finance

I used to have a larger portfolio at finnish Fellow Finance but I did not want to go below 12% for 4 star Finnish consumer loans therefore I started withdrawing funds last year. In January the sale price collections paid tor Finnish loans dropped from 70% to 53% which reinforced my decision to exit.

October

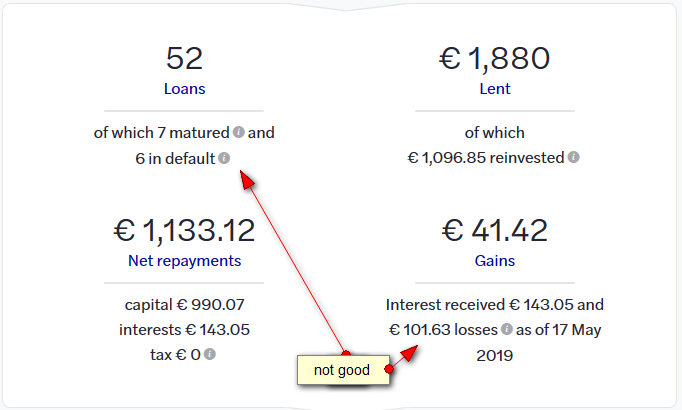

I am running down my portfolio on French SME loan marketplace October. With the low interest rates and rising defaults (6 out of 52 loans) in my portfolio the risk reward ratio is not for my taste anymore.

New investors signing up on October using this link* can get 20 EUR bonus (200 Euro minimum investment)

More p2p lending marketplaces

Due to professional interest (want to gain first hand experience) and curiosity I have more p2p lending portfolios at Ablrate* (small, reinvesting), Assetz Capital* (tiny, reinvesting, possibly increasing), Bulkestate* (tiny, testing), Crowdestate* (small, reinvesting), Finbee* (tiny, nearly exited), Investly (small, reinvesting), Lenndy* (tiny, watching), Monestro, (tiny, exiting), Moneything* (small, exiting), Neofinance* (small, testing, probably running down), Reinvest24* (small, testing), Robocash* (small, reinvesting), Zlty Melon* (tiny, exiting next month when terms are up).

Crowdinvesting

Not p2p lending but investing in startups. I am a huge fan of Seedrs*. Investing in startups is of course even higher risk than investing in p2p lending. Nevertheless I went ahead and built a big Seedrs portfolio over the last years. Snapshot:

P2P Conference Riga

I am looking forward to be at the P2P Conference in Riga* which is less than 4 weeks away. The conference is reasonably priced (enter promotional code P2PEARLYBIRD40 for 40% rebate) and Riga can be reached with cheap flights from many European cities. BTW, Riga is an interesting town, if you have not been there yet you could combine the conference with some sightseeing.

Ratesetter is the brand name of one of the top 3 UK p2p lending marketplaces. Unfortunately only UK investors can invest on Ratesetter UK, otherwise I would have tried it out.

Ratesetter is also the brandname of Ratesetter Australia. While not rund by the same company this Australian p2p lending marketplace uses the same technology base and is offering similar products, consumer loans of up to 5 years. Since launching in 2014 Ratesetter Australia has originated more than 325 million AUD in loan.

The site does not feature it, but actually Ratesetter is open to non-resident investors. I recently found this out and went ahead and opened I account in the past week. The signup process for non-residents is not as straightforward as on other marketplaces. I post a detailed description of how I did it below.

But why send money that far away?

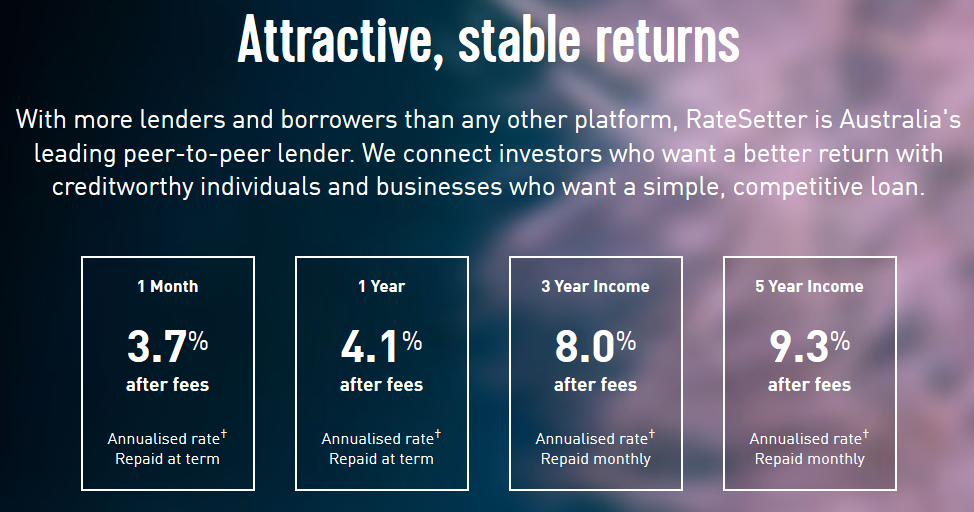

Because rates are attractive. Interest rates are currently up to 9.3% (compare that to around 6% that is achieveable for 5 year investments on Ratesetter UK*). And that rate is AFTER fees.

A further important feature is the provision fund. That is capital stored that is used to reimburse lenders of defaulted loans. While that is no insurance or guarantee, it is in my view a much stronger portection than the ‘buyback guarantee’ that some other market places promise.

There is currently 10.6 million AUD in the Ratesetter Australia provision fund. And since 2014 the provision fund has paid for every default without exception.

Review of advantages

established platform

very high interest rates (displayed rates are after fees)

no default losses since 2014 for investors (due to the provision fund)

comprehensive statistics & loanbook download

Review of disadvantages

signup a little more effort than usual (see description below)

no secondary market. Investors investing in the secondary market should not expect to be in a situation were they might need that money earlier

10% withholding Tax for German residents (for other countries check here – according to Ratesetter it is either 0% or 10% depending on country)

very volatile currency exchange rate

transaction fees for changing EUR -> AUD according to description below is 0.35%; to convert back AUD -> EUR the fee is 0.45%

My conclusion

Only investors that want to invest a larger amount for a long duration should consider this. Otherwise it is not worth the effort in my opinion.

Currency exchange rates EUR/AUD last five years (Source)

How I signed up as a a non-resident investor on Ratesetter Australia – step my step explanation

As the process is more effort than usual, I suggest you read the complete remainder of the article and decide if it is for you, instead of just diving into the registration process.

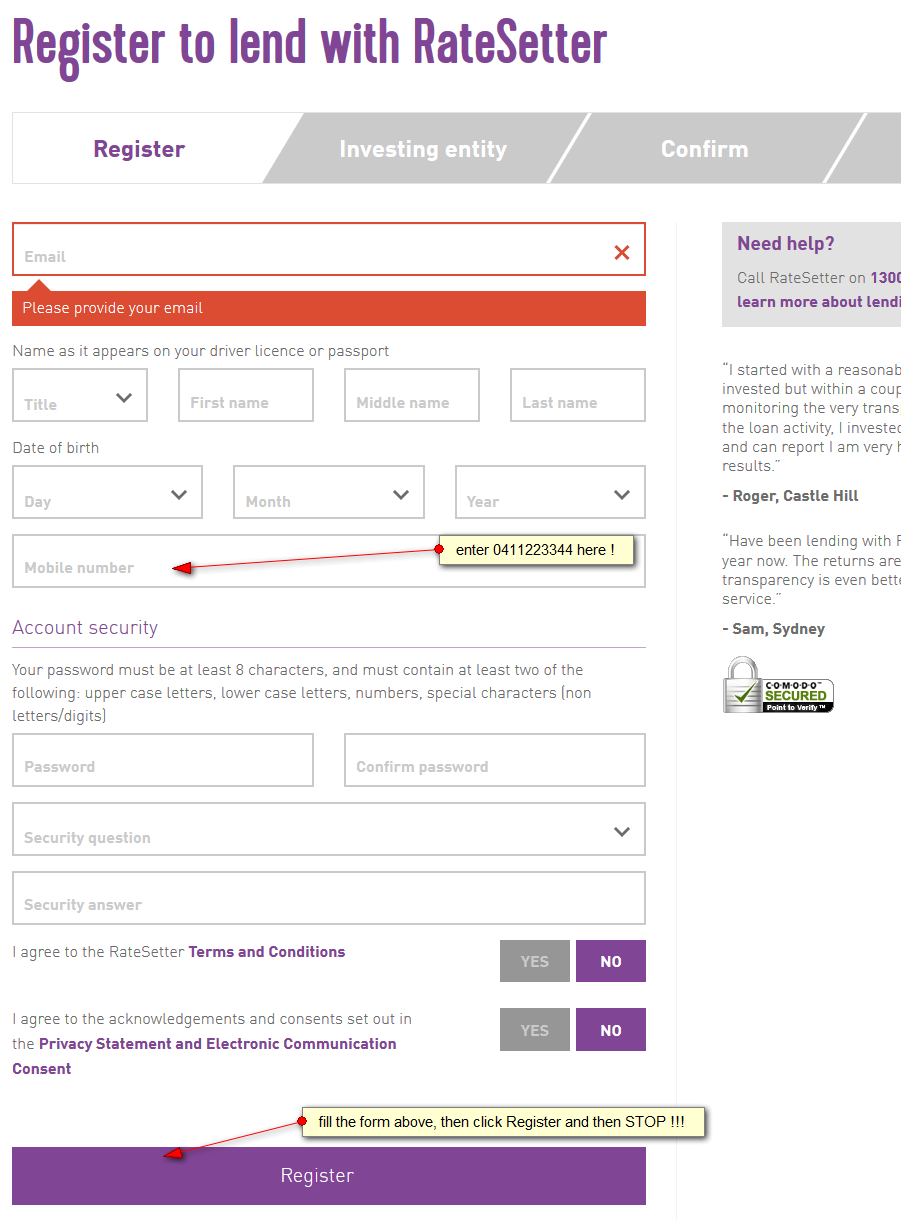

Step 1: Trigger Ratesetter registration process

Sign up via this link* and the first 5 investors have a chance to get a cashback bonus of $75 AUD – see conditions below*

First there is a welcome page, click “Register Now” there and then this page is shown:

Yes, you saw that right. After clicking Register, you STOP and do NOT proceed with the signup on the website as it can only handle Australian residents.

Step 2: Continue registration

After a few minutes I got an automated email asking me to complete my registration. I did NOT click on the link provided in the email, but rather send a reply email, stating that I am a German resident and would like to invest on Ratesetter and that I have an Australian bank account. I asked that they would please guide me through the process.

Step 3: Australian bank account

WTF? Sounds much more prohibiting than it actually is. I had a Transferwise* account already and with a few clicks could open a free Transferwise borderless account in Australian dollar which comes complete with account number and BSB code (routing code). If you don’t have Transferwise* you can open it for free, only plan a little time for verification.

The Australian Transferwise account later serves as reference bank account which is entered into the form in step 5.

Converting EUR in AUD costs 0.35% at Transferwise (how I saved that fees is written below). The current fee for later changing back AUD to EUR is 0.45%.

Step 4: Obtain scanned certified copies of documents for registration

While I waited for the answer from Ratesetter from Step 2, I went ahead and obtained scanned certified copies of documents. I could do that a the town hall (cost incurred 3.50 EUR). It will probably be different in other countries. Needed is a) current driver licence OR current passport b) proof of address no older then 60 days: utilities bill (such as an electricity bill or phone statement) OR bank statement or other bank correspondence OR correspondence from a local or central government department

Step 5:. Going on with registration

Meanwhile I got the reply from Ratesetter support. They are super helpful, but time zone difference means every back and forth takes a day. Ratesetter sent me a link of a web form to complete. I did that (entered ‘-‘ for SWIFT) and told them so via email, which I attached the requested certified document copies to.

Step 6: Registration is complete

One day later I got the confirmation that my registration was completed and I was ready to go.

Step 7: Deposit

One can now convert in the Transferwise account Euro to AUD wechseln and then send money from the Transferwise Australian currency account to Ratesetter. Ratesetter shows the necessary routing information under Transfer funds in > Transfer by Bank Transfer > Other

Saving in currency exchange when depositing

I could save the 0.35% Transferwise currency exchange fee for EUR > AUD by using a free Revolut* account and exchanging between Monday and Friday EUR to AUD fee free. Then transfer the AUD either to the Transferwise AUD account or directly as a Ratesetter deposit payment.

I just started. I intend to lend for the 5 year market and experiment with setting my own desired rates slightly above market rate. Watch out for an update here on the blog after I have several month of experience or – probably more frequently on the dedicated thread on the German discussion forum.

*$75 AUD Cashback Bonus for the first 5 investors, that register thought the given link before 16.09.2018 and at least $2000 AUDÂ on the 3 or 5 year market. Precise terms and conditions on the Ratesetter site. To qualify I think swift action will be needed, given that the registration, deposit and lending will take some time.

Auswide Bank Ltd (ASX:ABA) is increasing its equity stake in peer-to-peer lender MoneyPlace Holdings Pty Ltd (MoneyPlace). Auswide Bank will have a controlling interest of at least 51% in MoneyPlace with the prospect of increasing that interest up to 75% dependent on the final take up of other MoneyPlace shareholders in a capital raising initiative being undertaken by MoneyPlace.

MoneyPlace launched in October 2015 after receiving its retail and wholesale Australian Financial Services licence and provides loans of 5000 to 35,000 AUD through its peer-to-peer lending platform. Auswide Bank acquired a 19.3% equity stake in MoneyPlace in January 2016 while also committing funding to the Melbourne – based P2P lender’s consumer lending program.

Managing Director, Martin Barrett said Auswide Bank has been impressed with the platform, skills, capability and performance of MoneyPlace over the last 12 months, “Our funding has now exceeded 8 million AUD over the last 7 months and momentum continues to build. Loan quality has also been performing above expectations and we remain optimistic regarding future growth opportunities for the MoneyPlace and Auswide Bank partnership.â€

SocietyOne, an Australian p2p lending marketplace announced that it completed a 25M AUD round, supported by its existing shareholders. In 2014 Westpac owned Reinventure invested into SocietyOne. SocietyOne is led by CEO Jason Yetton, a former Westpac executive, who was appointed in March. The SocietyOne loanbook is currently over 100M AUD.