This is a guest post by Pawee Jenweeranon, a graduate school student of the program for leading graduate schools – cross border legal institution design, Nagoya University, Japan. Pawee is a former legal officer of the Supreme Court of Thailand. His research interests include internet finance and patent law in the IT industry.

1. Introduction : The Peer-to-peer Lending Industry in Thailand

Peer-to-peer lending which also known as social lending or crowd lending has drastically increased in the recent years in many countries over the world. The volume of peer-to-peer lending activities also has been grown rapidly, for instance, the volume of peer-to-peer lending activities in U.K. has doubled every year in the last four years.

Peer-to-peer lending might be used in many ways if it is properly regulated by the responsible authorities, this is one of the reasons which lead to the issuance of the consultation paper to regulate peer-to-peer lending industry by the Bank of Thailand.

For instance, due to the current situation, poor people and SMEs in Thailand normally face difficulties in accessing finance from banks or traditional financial institutions[i]. This affects the increasing number of informal loans outside the financial institution system which are normally illegal, specifically; the problem of informal loans currently stood at more than 5 trillion baht and covered around 8 million households in Thailand[ii]. Continue reading →

BLender, a p2p lending company from Israel, today announced its global expansion, beginning with new offices in Milan, Italy and Vilnius, Lithuania that will serve customers in Italy and the Baltics. The Israeli-based company delivers a P2P lending platform with a proprietary consumer credit rating system designed for territories without credit bureaus or traditional consumer credit information. BLender is a cloud-based platform that was built to work in a wide range of markets and languages.

In Italy the platform charges borrowers a 4.5% origination fee and investors 1.5% of each repayment (principal and repayment). Compared to other marketplaces these fees are in the higher price range. The fee for selling a loan on the secondary market is 0.45%.

BLender has experienced exponential growth since its launch in 2014 and has already provided approximately 12 million USD in loans. The company will continue expanding its global operations into territories that are craving consumer credit. In 2017, BLender plans to launch operations in Africa, Latin America and other European Union (EU) countries.

“Offering multi-national P2P lending has been our vision since BLender’s establishment,†said Dr. Gal Aviv, CEO, BLender. “Since our Israeli launch in 2014, we have built the foundation, infrastructure and technology to enable BLender to operate in the global market, so we will be able to face operating, cultural, technological, regulatory and taxation challenges.â€

With the expansion into Italy and the Baltics, BLender is enabling users to lend and/or borrow across countries, making financial borders a thing of a the past, says the service.

“BLender identified a credit gap in countries where the supply of consumer credit is insufficient for the populations’ needs and is priced very high, and a gap in other countries where the savings options have very low or even negative yield,†said David Blumberg, founder and managing partner, Blumberg Capital, a San Francisco-based venture capital firm that led BLender’s last funding round. “BLender’s multi-national lending options mediate this credit gap by creating a meeting ground between borrowers from countries that lack consumer credit, to lenders from countries where the yield on their savings in insufficient. We support and strongly believe in the vision, management capabilities and business potential of the BLender team.â€

Investors on the BLender platform will earn predicted interest rates of 5-6% annually. The safeguard fund acts as an additional layer of protection to the lenders in case of a default. BLender’s default rate is approximately 1% before activating the safeguard fund. Thanks to the SafeGuard fund, the effective default rate is 0% says the service. BLender also offers ReBlendTM, BLender’s secondary market that offers the lenders the option the trade their loan portfolios and enjoy liquidity.

Recently BLender was chosen to participate in the exclusive ELITE program of the UK Stock Exchange that finds and nurtures companies with the potential for an IPO. As part of the program, BLender receives the guidance of the program’s experts for two years that help promote the company’s activity.

Furthermore, the company was selected as one of the most promising Fin-Tech companies in the world for 2015 by the accounting firm – KPMG, and also by the United Kingdom Trade and Investment Department.

The multi-national expansion was done in collaboration with KPMG.

Silver Bullion Pte Ltd in Singapore reported today, on the anniversary of the launch of their bullion secured peer-to-peer(P2P) loan platform, that the platform has funded over S$11 million across more than 400 successfully matched loans. There were zero occurrences of borrowers defaulting on their loans. One hundred percent of lenders, with loan tenures expiring within the first year, received their principle with interest on time.

Launched on 5th August 2015, Silver Bullion offers a p2p marketplace that allows borrowers to obtain a loan using physical gold and silver bullion as collateral. This gives lenders, seeking a good rate of return, confidence that their investments are safe.

Silver Bullion’s CEO, Gregor Gregersen, commented: ‘The first year results of our P2P loan platform shows that owners of physical gold and silver like to have the option to be able to borrow short term funds at good rates with the bullion that they store with us. Now, they are able to reinvest with the borrowed funds whilst continuing to own bullion and benefit from rising gold and silver prices.’

P2P-Banking.com conducted an interview with Gregersen earlier this year.

Due to the safety that Silver Bullion’s loan platform gives to lenders, 72% of the matched loans were initiated by borrowers. The company has seen more than 30 loans matched consistently each month since March 2016 – a rate of more than 1 matched loan per day. Interest rates across all loan tenures currently hovers between 2.5% and 4.5% per annum. Unlike unsecured P2P lending platforms, loans matched by Silver Bullion’s lending platform are fully backed by physical gold and silver. Loans with tenures longer than 6 months begin with a collateral-to-loan value of 200%. The exceptions are loans with the 1 month tenure which have a lower collateral-to-loan value of 160%.<

Borrowers’ collateralized bullion is stored at Silver Bullion’s vault, The Safe House. They are covered by one of the most comprehensive insurance policies in the industry that also insures against inside jobs and any unexplained losses.

This is a guest post by Hungyi Chen, Ph.D. candidate at the Graduate School of Law, Nagoya University. He is researching alternative finance in East Asia.

1. Relevant Background

Internet finance, including (1) online stored payment by non-bank, (2) crowdfunding and (3) peer-to-peer lending becomes hotly debated issues in Taiwan recently. To boost the development of financial innovation, the regulation of online stored payments by non-banks was already implemented on January 2015 after discussions and debates between financial authority and platforms. Besides, a regulatory framework for equity-based crowdfunding has also been enacted in the end of April 2015 and amended in the early of January 2016.

In order to encourage and accelerate the development of fintech industry in Taiwan, the financial authority, Financial Supervisory Commission (FSC) of Taiwan, has published Fintech Development Strategy White Paper on May 2016[i]. One of main goals is evaluating the possibility of introducing the mechanism of P2P lending into Taiwan’s capital market and providing a regime for regulating this industry.

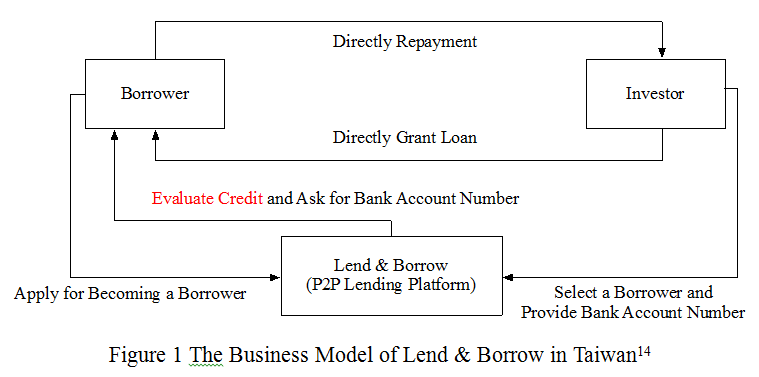

Some business models of P2P lending are forbidden due to conflict with The Banking Act[ii] in Taiwan. Recently, it is considered to be introduced in Taiwan and evaluated by the recently established project team of the financial authority in Taiwan, Financial Supervisory Commission (FSC)[iii]. Despite the fact that the attitude toward P2P lending industry of financial authority in Taiwan is still vague, as of July 2016 there are three P2P lending platforms already providing their services in Taiwan, including Lend & Borrow[iv], Wow88[v], XiangMinDai[vi]. They have tried to design their business model to avoid potential legal risks. For better understanding of the P2P lending industry, this article tries to provide a brief regulatory overview of Taiwan in following part.

2. Regulatory Overview of P2P lending

Currently, there is no any specific regulation toward this industry in Taiwan. Recent official document[vii], indicate that the business model of P2P lending in Taiwan should avoid to involve in any activities of accumulating capital from general public or issuing any securities. XiangMinDai, a P2P lending platform in Taiwan, has analyzed by FSC of Taiwan. The former chairman of FSC of Taiwan, Ms. Wang, has stated that ‘…the business model of XiangMinDai is majorly providing services of debt transaction, which does not involve in activities of depositing or charging fund. Accordingly, it is not the regulatory scope of FSC at this moment…[viii]‘

Although there is no any financial regulation of P2P lending in Taiwan, Banking Bureau of FSC has issued a statement[ix] on April 14, 2016, pointing out some legal compliance issues for P2P lending platforms, including (1) platforms should not involve in issuing any securities, (2) ensure privacy of customers, (3) activities of deposit and store-value business without licenses are forbidden, (4) illegal ways of debt-collection is forbidden.

Within 2 weeks, Banking Bureau of FSC, announced another statement[x] for supplement, indicating that (1) the interest rates of the case on the P2P lending platform is 30.15%, which may be illegal according to Criminal Act in Taiwan[xi], (2) legal concern of breaking the law of Multi-Level Marketing Supervision Act[xii] and Fair Trade Act[xiii]. Continue reading →

This is a guest post by Hungyi Chen, Ph.D. candidate at the Graduate School of Law, Nagoya University. He is researching alternative finance in East Asia.

1. The recent development of online alternative finance

Given the recent trend that Fintech is rapidly growing in the world, in order to maintain the role of international financial center, the financial authority of Hong Kong has been aware of issues relating to Fintech industry[1]. On November 13th, 2015, Stored Value Facilities Payment Systems, such as online stored payment business as PayPal, is allowed to operate by non-bank[2]. This is a milestone for Hong Kong including non-bank of operating business highly relevant to conventional bank.

In order to enhance the development of startups in Hong Kong, financial technologies (Fintech) are emphasized by the authority since the investment of Fintech is a target of many venture capitalists[3]. Nevertheless, compared with other jurisdictions in Asian countries, which already lightened entry requirement to encourage non-bank for engaging business of equity-based crowdfunding, such as Japan, Korea, Malaysia, Taiwan, and Thailand, the entry requirement of Fintech, especially alternative finance may be stricter in Hong Kong.

Until now, there is still no equity-based crowdfunding platform established in Hong Kong. However, the huge demand from capital market gradually leads the development of crowdfunding in Hong Kong, especially debt-based crowdfunding, which is also known as Peer-to-Peer Lending. Currently, there are 4 major peer-to-peer lending platforms, including BestLend, GoLend, Monexo, and WeLend.

2. Relevant industry background

With unique selling factors, the peer-to-peer lending platforms may have a rapid growth in the near future. On one hand, from viewpoints of investors, the deposit rates of savings are from 0%~0.001%[4]. Even the deposit rates of fixed deposit of 12 months are from 0.15%~0.2%[5]. Additionally, inflation rates are around 4% continuously in 2013 and 2014[6], which means the real interest rate may be negative in Hong Kong. Accordingly, there are strong incentives for investors to vitalize their capital.

On the other hand, from viewpoints of borrowers, there are two fundraising channels for loans, including banks (Licensed Banks, Restricted License Banks, Deposit-taking Companies) and Money Lenders. Since the financial authority restricted the mortgage market of banks to prevent a real-estate bubble, it is difficult for borrowers to get the loan amount they need from banks by mortgage. As a result, they turn to Money Lenders as an alternative opportunity. Although the interest rates of Money Lender are generally higher than banks, compared with banks which normally take 1-6 weeks for examining procedure, the process of Money Lender is more simplified[7]. Continue reading →

This is a guest post by Pawee Jenweeranon, a graduate school student of the program for leading graduate schools – cross border legal institution design, Nagoya University, Japan. Pawee is a former legal officer of the Supreme Court of Thailand. His research interests include internet finance and patent law in the IT industry.

1. Introduction

In the recent years, it is inevitable that the financial technology or Fintech takes the significant role toward the evolution of financial services industry in this region. In other words, Fintech normally be used to improve the financial industry services.

In 2015, the Monetary Authority of Singapore (hereinafter referred to as “MASâ€) has committed two hundred twenty five million Singapore Dollar (around 166 million USD) to support the development of Fintech industry for the startup ecosystem in the upcoming years[1]. This is a good reflection of the significance of the financial technology or Fintech development in Singapore.

From the economic perspective, Small and Medium Enterprises (hereinafter referred to as “SMEsâ€) are important part of Singapore’s economy. SMEs account for 99 percent of all registered enterprises in Singapore[2]. From this reason, enhancing the competitive capacity of Singapore SMEs is essential for Singapore economy development.  Even almost all of the SMEs in Singapore are supported by the Governmental Enterprise Development Agency and Centers[3], (more than 100,000 SMEs got funding support by the Singapore government[4]); however, internet financial technology was also proposed as an alternative mechanism for enhancing the competitiveness of Singapore SMEs in the recent years[5].

2. Regarding Peer to Peer Lending

2.1 Background Generally, there are many peer to peer lending platforms in Singapore; however, they normally lend money to businesses rather than individuals due to the strict regulation for money lenders. The additional limitation on lending to low-income borrowers[6] who are Singaporean citizens or permanent residents which is another requirement should be considered by the lenders.

In general, money lending in Singapore is mainly regulated by the Moneylenders Act 2010 and the Moneylenders Rules 2009. For the Moneylenders Act 2010, due to the main purpose of this act is to develop consumer protection mechanism to protect borrowers of small amount loans[7], this is the reason why the act provides stringent limitation for moneylenders to operate their business. This is another key different of money lending law of Singapore compared to other countries in Asia such as Hong Kong which focusing more on lending activity[8]. Briefly, the act requires moneylenders to hold the Moneylenders license with obligations and limitations for licensee[9].

In Singapore, even there are strict regulations in the existing law relating to a money lending business; however, there is the legislative effort of the Singapore government to address the issue regarding Securities-based Crowdfunding, which can reflect the understanding of the Singapore government toward the development of Financial Technology (Fintech) and the supporting regulatory framework.[10]

2.2 TheRegulatory Framework for Peer to Peer Lending Business

From the document published by the MAS on Lending-based Crowdfunding – Frequently Asked Questions (FAQs)[11], generally, the operation of P2P lending is restricted by MAS under the Securities and Futures Act (Cap. 289) (SFA) and the Financial Advisers Act (Cap. 110) (FFA).

Specifically, the P2P lending business needs to prepare and register a prospectus with MAS in accordance with Section 239(3) of the SFA. In addition, not only the registration of the prospectus but also the P2P lending platform need to follow the licensing requirements, particularly, the P2P lending business which fall within the scope provided by MAS needs to hold a Capital Market Services (CMS) license. Continue reading →