Compared to the beginning of July the interest rates for newly issued EUR loans on Mintos are much lower now. While investors enjoyed interest rates of up to 13-14% for loans issued in the first half of the year, typical rates are 8-11% now, with a 12-13% for more exotic loans mixed in.

Cause of the change in market condition was that Mogo, one of the larger loan originators on Mintos, issued a bond worth EUR 50 million, with an annual interest rate of 9.5% (ISIN XS1831877755) on June 25, 2018 and Mogo announced that starting from July 13, 2018, Mogo would partially repurchase loans from investors on Mintos using their call option as stipulated in the assignment agreement. During July, Mogo plans to gradually repurchase in total up to EUR 16 million net of loans issued to borrowers in Bulgaria, Estonia, Latvia, Lithuania, Poland, and Romania.

Following the repurchase, the interest rates for newly issued EUR loans were sharply lower not only for Mogo loans but also for loans of the other originators on the Mintos platform.

This left most investors with a lot of cash in their accounts, as commonly 1/3 to 2/3 of all the Mogo loans in their portfolios had been repurchased and their previously configured autoinvests did not match any loans any more at their set interest rates.

To find out how investors reacted to the situation P2P-Kredite.com conducted a survey among German speaking Mintos investors. Here are the preliminary results (48 respondents):

35% say they withdraw uninvested cash and invest it on other p2p lending platforms

21% say they continue to invest on Mintos primary market

17% say they just wait, the interest rates will rise again

15% say they withdraw uninvested cash and invest it in other asset classes (e.g stock)

12% say they buy on the Mintos secondary market now, instead of using the primary market

For continental European investors looking for high yield alternatives here are 5 platforms that survey respondents liked:

Bondora Bondora is a long established Estonian company offering consumer loans in Estonia, Finland and Spain. Investors can choose between their new “Go&Grow” product (up to 6.75% interest) or the self-select autoinvest options with individual loans yielding much higher (nominal) interest rates

Estateguru Estateguru is a marketplace for property secured loans mostly in the baltic countries. Typical interest rates are 10-12%. Investors pick individual loans or enable autoinvest

Grupeer Grupeer is a young Latvian platform gaining popularity among the German investors. They list business and development loans in several countries (e.g. Latvia, Russia, Belarus, Norway, Poland). Typical interest rates are 14-15%

Peerberry Peerberry is a young Latvian platform listing consumer and property loans in several countries (e.g. Lithuania, Poland, Czech Republic, Ukraine). Typical interest rates are 11-13%

Robocash Robocash is a Latvian platform listing consumer loans in Kazachstan and Spain. Typical interest rates are 14-14.5%.

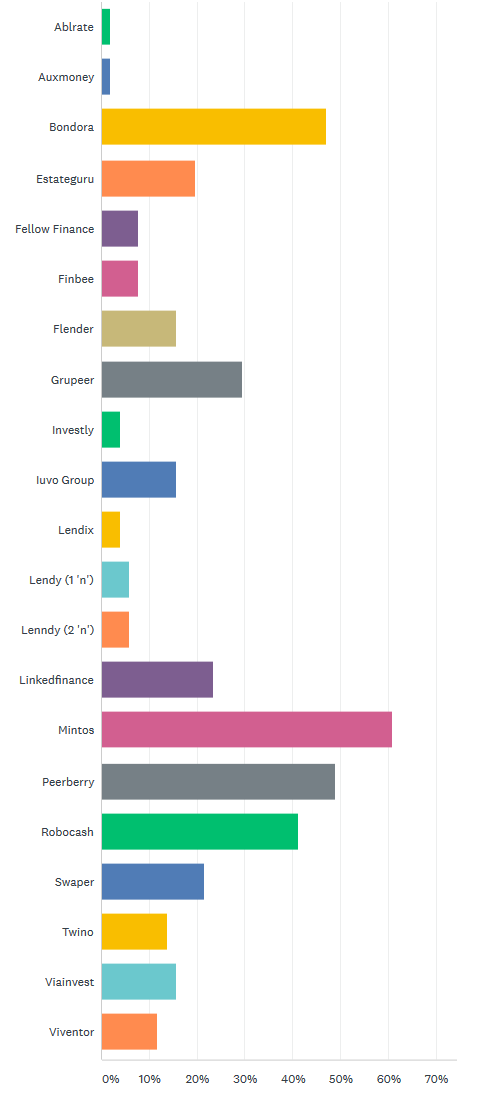

This selection is based on the likings of German speaking investors that voted in August for best p2p lending platform in a P2P-Kredite.com survey:

51 respondents, platforms that got no votes are not shown

The survey shows that Mintos is still rated number one in investor opinion among the queried audience, but the others are catching up (compared to similar surveys in the past).

My own Mintos portfolio shrank to less than 40% of its previous size as only less than 1/3 of the Mogo loans I had in early July are still in my portfolio. I withdrew a lot of cash and have transfered it to other p2p lending market places. Of course I’ll hold on to the my remaining Mogo loans as nearly all of them are at 13-14% interest rate.

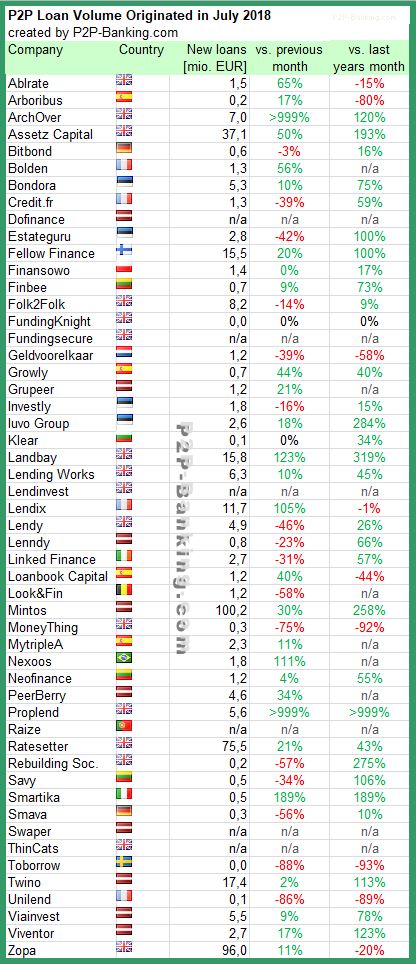

The table lists the loan originations of p2p lending marketplaces for last month. Mintos leads ahead of Zopa and Ratesetter. . The total volume for the reported marketplaces listed in the table adds up to 449 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

The table lists the loan originations of p2p lending marketplaces for last month. Zopa leads ahead of Mintos and Ratesetter. I delisted Funding Circle from the table as they announced they will only update figures quarterly now (was daily). Furthermore they have withdrawn the downloadable loanbook. The total volume for the reported marketplaces listed in the table adds up to 380 million Euro. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms.

Milestones achieved this month (overall volume since launch):

BDO has prepared and emailed the Joint Adminstrators’ Proposal to investors and creditors of the Collateral Companies last night. The report is also available publicly on the BDO website. I have read the whole report. I will not attempt to summarize it, but point out some findings that I find personally really surprising given that Collateral was an operation that managed millions of pounds of client money.

From the outset of the Administrations, we identified that securing the Companies’ electronic records would be critical. Following our initial meeting, the directors advised that all of the Companies’ IT functions and services were outsourced to an IT consultant. Both the directors and … advised that they had no access to the electronic platform, nor any back-up of the data contained within it, and they advised that the electronic platform had been decommissioned during March 2018 due to non-payment of outstanding bills; they did not therefore consider that the Joint Administrators would be able to recover the platform or the underlying data

The company outsourced IT operations, but kept no copies or backups of the data stored. Wow.

BDO did not give up on this, but located the servers and data forensics are working on recovering (part) of the data.

We have since made contact with the third party company holding the servers. Again, following protracted correspondence and with the assistance of our lawyers and my firm’s Forensic Technology team, we have located and secured the actual servers previously used by the Companies. There appears to be a significant volume of data still held on those servers and, as at the date of these proposals, we have taken steps to consolidate the contents of the different servers containing the Companies’ data into a single location (whilst preserving the originals intact). We shortly expect to receive a copy of the data, which we will then interrogate and review to better understand the nature of the data that has been recovered. Whilst it is not yet clear whether we have retrieved all of the Companies’ electronic data, nor whether it will be possible to restore the electronic platform, the Joint Administrators consider that this represents positive progress.

Given that the allocation of client money to loans and the bookkeeping is a primary tasks of a p2p lending marketplace I am appalled when I read this finding:

… also provided certain key information in relation to the investors and loan book, in the form of two spreadsheets (which I refer to below) and copies of email correspondence between his office and various stakeholders during the period in which he purported to act as administrator. …advised that he held no other books or records, and neither did he have any access to the Companies’ electronic platform, or the data contained within it.

Really? The data was held in two spreadsheets? Excel, maybe?

A last quote (highlighting is mine)

Members of the Joint Administrators’ team attended the Companies’ trading address in Manchester on the afternoon of their appointment. The address is a serviced office space, and the office provider advised that the Companies had vacated the office several months prior to the Joint Administrators’ appointment. There were no assets or books and records remaining at the premises.

Now to the good news. BDO confirmed there is money in the client and office accounts. And the report shows the directors are cooperating with the administrator. The report seems to classify investor’s money as trust assets which would, as I understand it, leave investors in a much better position, than the outcome would have been, if they would have been qualified as pure unsecured creditors.

BDO says it is too early to give a forecast to the outcome, given the circumstances, but asseses:

We would, however, note that, as summarised on the statement of estimated financial position attached at Appendix 2, the estimated claims of creditors exceed the book value of the assets held by the Companies (including trust assets). Therefore, even before taking account of any potential asset write-downs and the costs of the Administrations, it appears likely that not all investors and creditors will recover their entire exposure to the Companies and the Collateral lending platform.

A lot will depend on how much can be retrieved from the outstanding property loans, which will fall due by mid-November 2018 at latest.

There is a lot of investor discussion regarding the report on the P2pindependentforum.

Trying to look at this from a high vantage point:

In my opinion a lot of the work, time and fees of BDO would have been saved, if the data would have been stored more persistently by Collateral in the first place

Investors should try to keep some form of offline records. I know depending on platform and number of loans that might be hard and laborous to do, but look at what position the Collateral investors are in now. It is uncertain though if those investors that do have precise records on their loan allocation will be in any way better off than those that do not in the Collateral case

Investors trust regarding operations stability and bookkeeping of smaller UK platforms (Collateral had 5 employees) may be dealt a blow. It might become more important for smaller UK marketplaces to demonstrate robustness and durability of operations (e.g. through a detailed and transparent documentation of the living will, which is required for fully authorised platforms anyway)

The next steps in the Collateral case are described in the proposals in 15.1. and 15.2 of the report (page 20).

Alla Kisika: Grupeer is all about people! We have created the platform which is based on 3 pillars:

Security (protection)

Technologies (efficiency)

Benefit (profitability)

Our platform is not just the bridge connecting the borrower and the investors, Grupeer is a transparent environment in which the investors can feel safe, receiving fast and clear high profit, using the latest technologies.

What are the three main advantages for investors?

Vladislav Filimonov: As mentioned, the financial safety of our investors is our main priority. First of all, the number of outstanding or default transactions it is equal to zero. This indicator is reached only to our rigid scoring which eliminates nearly 75% of the loan originators interested to place the projects on our platform. The reverse side of the coin is lack of variety of the projects.

Secondly, we give a unique opportunity to diversify the portfolio, investing in business loans or in development projects within one platform.

And last but not least, all of our loan originators provide BuyBack guarantees for each project. Besides, our investors get access to all financial information of the borrower of the project. To convince of our advantages, we offer the minimum sum of the contribution of 10 EUR, we are sure that after the first experience, the investors will become our loyal customer!

As for development projects, in many scenarios, the management members of Grupeer are acting as a shareholder to have a full control towards successful implementation of it.

What are the three main advantages for borrowers?

Alla Kisika: To clarify, Grupeer doesn’t issue the credits and we are working with legal entities only.

“Fuel for your business.†The borrower has a possibility of refinancing due to the services of our platform, and it means that, the company will get the financial resources or as we call it – fuel to grow the company at the velocity of the rocket.

The size doesn’t matter. We consider borrowers of all sizes. And experience has shown that size doesn’t matter. Even if the borrower is small, but with good financial history, we are ready to provide favorable credit rates, fast result and high-quality services to grow together!

Great Customer Experience. We are sure that services and the ideas can be copied but what really distinguishes is the way the service is provided. Customer satisfaction is our Top priority. We practice the individual approach to each partner from the beginning to the very end.

What ROI can investors expect?

Alla Kisika: We can proudly say that now the average net annual return of Grupeer is 14.25% and it is the highest annual average rate on the market. Most of our projects have the stable interest rate of 14%, some of them, for example, the most loved by German investors- Finsputnik Platforma SIA projects have 15% interest rate.

It should be mentioned that there is no correlation between a high interest rate and the increased risk. Such high-interest rate is stipulated by company’s policy and marketing strategy which makes our platform attractive to check the mechanism of return of percent and principal.

Grupeer offers a wide variety of loans from several countries. How do you succeed in sourcing and checking these loans?

Vladislav Filimonov: As mentioned above, we don’t offer a wide range of the loans from the different countries but considering that we could critically improve our scoring system that pays off for 100% (we would like to remind that the number of expired and default transactions is equal to zero). Besides, our sales team started to work on attracting the new projects therefore soon we will please our investors with many new projects.

How did you get the idea to launch a p2p lending marketplace?

Alla Kisika: Life gave the idea of the platform development. In due time, the founders of the platform had a very serious project regarding the construction and commissioning of the Thermal power plant. At some point, when a large amount of financial means has been already invested and very little remained before the end of the project, the need of additional 3 million euros has appeared. Founders have faced a problem of the full amount as someone wanted to invest only 500’000 EUR, someone 1’500’000 EUR and these people were not friendly with each other therefore a certain sum of money hasn’t been collected till the deadline and the project was closed. And the conclusion was obvious –  human relationship shouldn’t influence implementation of the projects and that it is necessary to develop the platform which will provide such an opportunity. And Grupeer platform has been developed for this purpose.

Can you please tell us a bit about your background and the team’s background?

Vladislav Filimonov: Force and success of our company is our employees. From myself, I have gained a massive experience in leading Large Group of Multinational Teams as a Vice-President of Mastercard and while working in Pay Pal. This experience is now spread across all functions of Grupeer to make it even more investors-oriented platform.

Below you can meet some of our team members:

CEO – Andrey Kisiks is the professional developer with 20+ years of experience in European Union. Fields of activity: construction, residential real estate projects development, construction and operational commissioning of complex technical objects (Power Supply), Finance and Peer-to-Peer.

CMO – Leonid Tenkaluk is experienced Digital Marketing Manager with a demonstrated history of working in the information technology and sales industry. Skilled in Team Management, Marketing Management, Negotiation, E-commerce and Entrepreneurship.

We very thoroughly select our employees, as our loan originators. In April of this year, several strong experts joined our team, and, in a few months, we are planning to double the number of our teammates to boost our team and to be able to go from “good†to “great.â€

Is the technical platform self-developed?

Vladislav Filimonov: Yes, our technical platform is 100% self-developed without using some “ready-to-use†software products. Besides that, we did not use any outsourcing services. The basic part of the platform is developed, but we continue to improve it on daily basis. We are planning to add several innovative solutions for the more convenient use of our platform in near future.

How is the company financed? Is it profitable?

Alla Kisika: The company is self-financed. As we have only started to conquer financial oceans, we didn’t manage to generate profit yet, but we are planning to reach a break-even already in the next year.

What were the main challenges when launching your platform?

Alla Kisika: As in any innovative field under that is not regulated by law we have faced several the bureaucratic issues which we are solving successfully. Secondly, we have spent a lot of time on development of the reliable scoring system to minimize any investor’s risks. And the main challenge today is to get our values over to the audience and to earn its trust.

Is Grupeer open to international investors?

Vladislav Filimonov: Yes, we are. Now, we work with investors who are EU residents. Soon, we will certainly expand our geography.

Where do you see Grupeer in 3 years?

Vladislav Filimonov: Our main objective in following 3 yeas is to become a leader service provider of the alternative investment market in EU. We don’t want to open plans prematurely, but we are planning to become the conductor to unique products in this market. To prove ourselves as the most innovative, safe and favourable platform.

You have one wish, that the regulator will fulfil. What is your wish?

Vladislav Filimonov: As they say – be careful what you wish for, you may receive it. Our sole ambition is the liberal relation to this field as P2P business is very perspective alternative for World economy.

P2P-Banking.com thanks Alla Kisika and Vladislav Filimonov for the interview.

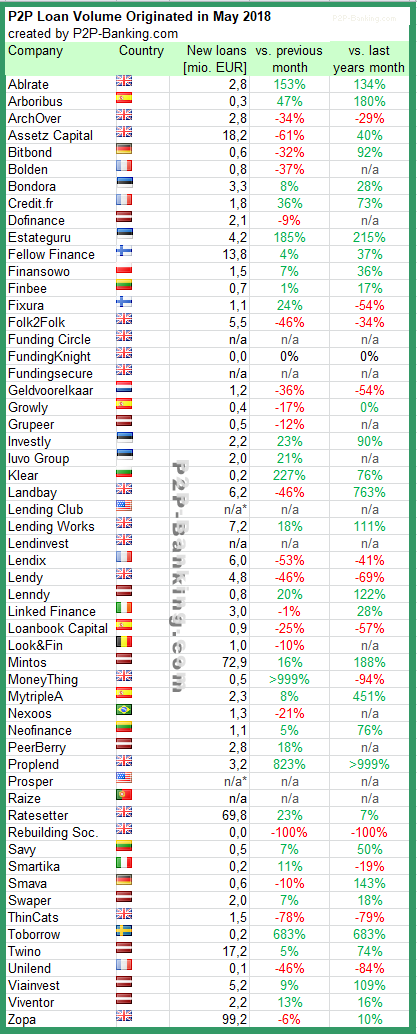

The table lists the loan originations of p2p lending marketplaces for last month. With the most recent Funding Circle figures not available at the moment, Zopa leads before Mintos. I track the development of p2p lending volumes for many markets. Since I already have most of the data on file, I can publish statistics on the monthly loan originations for selected p2p lending platforms. This month I added Grupeer.

Milestones achieved this month (overall volume since launch):

Table: P2P Lending Volumes in May 2018. Source: own research

Note that volumes have been converted from local currency to Euro for the purpose of comparison. Some figures are estimates/approximations. *Prosper and Lending Club no longer publish origination data for the most recent month.