It’s important to work for a company that you respect and provides a product good for its customers. It’s classic dinner table question, “what do you do for a livingâ€.  Mostly I’ve always worked for large blue chip companies including Standard Chartered Bank, PriceWaterhouseCoopers, Centrica, FICO, MasterCard and Lloyds Banking Group. So although I wasn’t going to set any dinner party conversations alight, I didn’t have to admit I worked as an estate agent, politician or worse. Then I worked with RateSetter and I became actually proud of my employment, what’s not to like about working for an internet start-up in something funky called “peer-to-peerâ€. I was helping to provide a better product to a new type of investor called a “lender†in a new asset class that was providing fair and consistent returns. We were bringing a new lexicon to banking and innovations such as the Provision Fund. Borrowers also got a better deal from a company with excellent customer service, not disdain. I wasn’t a banker anymore, I was working in the “sharing economyâ€, a financial hipster….

However I’ve been lucky to have these employment choices. I’ve been the first cynic to sit on his pedestal and mock those that worked for less altruistic companies. And when I met people working for high-cost short-term lenders, I never let them forget it. I wasn’t a supporter of the football clubs that took their money to advertise a terrible product on their shirts. This is especially personal as I have a family interest, someone that isn’t so financially literate (and to be blunt, who was in dire straits) that borrowed 300 GBP, and ended up having to pay back 1,200 GBP within nine months. As far as I was concerned the sub-prime pay-day loan industry had a poor reputation for a reason, some lenders were exploitative. I mean, can anyone really defend 5,000% APRs? So why have I agreed to work for a short term lender, The Money Platform. A few of my friends are already looking down on me from that moral pedestal that I previously sat upon. Continue reading →

This is a guest post by Pawee Jenweeranon, a graduate school student of the program for leading graduate schools – cross border legal institution design, Nagoya University, Japan. Pawee is a former legal officer of the Supreme Court of Thailand. His research interests include internet finance and patent law in the IT industry.

1. Introduction : The Peer-to-peer Lending Industry in Thailand

Peer-to-peer lending which also known as social lending or crowd lending has drastically increased in the recent years in many countries over the world. The volume of peer-to-peer lending activities also has been grown rapidly, for instance, the volume of peer-to-peer lending activities in U.K. has doubled every year in the last four years.

Peer-to-peer lending might be used in many ways if it is properly regulated by the responsible authorities, this is one of the reasons which lead to the issuance of the consultation paper to regulate peer-to-peer lending industry by the Bank of Thailand.

For instance, due to the current situation, poor people and SMEs in Thailand normally face difficulties in accessing finance from banks or traditional financial institutions[i]. This affects the increasing number of informal loans outside the financial institution system which are normally illegal, specifically; the problem of informal loans currently stood at more than 5 trillion baht and covered around 8 million households in Thailand[ii]. Continue reading →

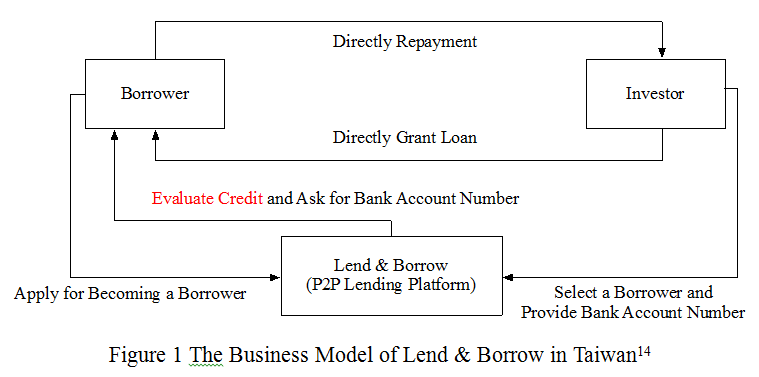

This is a guest post by Hungyi Chen, Ph.D. candidate at the Graduate School of Law, Nagoya University. He is researching alternative finance in East Asia.

1. Relevant Background

Internet finance, including (1) online stored payment by non-bank, (2) crowdfunding and (3) peer-to-peer lending becomes hotly debated issues in Taiwan recently. To boost the development of financial innovation, the regulation of online stored payments by non-banks was already implemented on January 2015 after discussions and debates between financial authority and platforms. Besides, a regulatory framework for equity-based crowdfunding has also been enacted in the end of April 2015 and amended in the early of January 2016.

In order to encourage and accelerate the development of fintech industry in Taiwan, the financial authority, Financial Supervisory Commission (FSC) of Taiwan, has published Fintech Development Strategy White Paper on May 2016[i]. One of main goals is evaluating the possibility of introducing the mechanism of P2P lending into Taiwan’s capital market and providing a regime for regulating this industry.

Some business models of P2P lending are forbidden due to conflict with The Banking Act[ii] in Taiwan. Recently, it is considered to be introduced in Taiwan and evaluated by the recently established project team of the financial authority in Taiwan, Financial Supervisory Commission (FSC)[iii]. Despite the fact that the attitude toward P2P lending industry of financial authority in Taiwan is still vague, as of July 2016 there are three P2P lending platforms already providing their services in Taiwan, including Lend & Borrow[iv], Wow88[v], XiangMinDai[vi]. They have tried to design their business model to avoid potential legal risks. For better understanding of the P2P lending industry, this article tries to provide a brief regulatory overview of Taiwan in following part.

2. Regulatory Overview of P2P lending

Currently, there is no any specific regulation toward this industry in Taiwan. Recent official document[vii], indicate that the business model of P2P lending in Taiwan should avoid to involve in any activities of accumulating capital from general public or issuing any securities. XiangMinDai, a P2P lending platform in Taiwan, has analyzed by FSC of Taiwan. The former chairman of FSC of Taiwan, Ms. Wang, has stated that ‘…the business model of XiangMinDai is majorly providing services of debt transaction, which does not involve in activities of depositing or charging fund. Accordingly, it is not the regulatory scope of FSC at this moment…[viii]‘

Although there is no any financial regulation of P2P lending in Taiwan, Banking Bureau of FSC has issued a statement[ix] on April 14, 2016, pointing out some legal compliance issues for P2P lending platforms, including (1) platforms should not involve in issuing any securities, (2) ensure privacy of customers, (3) activities of deposit and store-value business without licenses are forbidden, (4) illegal ways of debt-collection is forbidden.

Within 2 weeks, Banking Bureau of FSC, announced another statement[x] for supplement, indicating that (1) the interest rates of the case on the P2P lending platform is 30.15%, which may be illegal according to Criminal Act in Taiwan[xi], (2) legal concern of breaking the law of Multi-Level Marketing Supervision Act[xii] and Fair Trade Act[xiii]. Continue reading →

This is a guest post by Hungyi Chen, Ph.D. candidate at the Graduate School of Law, Nagoya University. He is researching alternative finance in East Asia.

1. The recent development of online alternative finance

Given the recent trend that Fintech is rapidly growing in the world, in order to maintain the role of international financial center, the financial authority of Hong Kong has been aware of issues relating to Fintech industry[1]. On November 13th, 2015, Stored Value Facilities Payment Systems, such as online stored payment business as PayPal, is allowed to operate by non-bank[2]. This is a milestone for Hong Kong including non-bank of operating business highly relevant to conventional bank.

In order to enhance the development of startups in Hong Kong, financial technologies (Fintech) are emphasized by the authority since the investment of Fintech is a target of many venture capitalists[3]. Nevertheless, compared with other jurisdictions in Asian countries, which already lightened entry requirement to encourage non-bank for engaging business of equity-based crowdfunding, such as Japan, Korea, Malaysia, Taiwan, and Thailand, the entry requirement of Fintech, especially alternative finance may be stricter in Hong Kong.

Until now, there is still no equity-based crowdfunding platform established in Hong Kong. However, the huge demand from capital market gradually leads the development of crowdfunding in Hong Kong, especially debt-based crowdfunding, which is also known as Peer-to-Peer Lending. Currently, there are 4 major peer-to-peer lending platforms, including BestLend, GoLend, Monexo, and WeLend.

2. Relevant industry background

With unique selling factors, the peer-to-peer lending platforms may have a rapid growth in the near future. On one hand, from viewpoints of investors, the deposit rates of savings are from 0%~0.001%[4]. Even the deposit rates of fixed deposit of 12 months are from 0.15%~0.2%[5]. Additionally, inflation rates are around 4% continuously in 2013 and 2014[6], which means the real interest rate may be negative in Hong Kong. Accordingly, there are strong incentives for investors to vitalize their capital.

On the other hand, from viewpoints of borrowers, there are two fundraising channels for loans, including banks (Licensed Banks, Restricted License Banks, Deposit-taking Companies) and Money Lenders. Since the financial authority restricted the mortgage market of banks to prevent a real-estate bubble, it is difficult for borrowers to get the loan amount they need from banks by mortgage. As a result, they turn to Money Lenders as an alternative opportunity. Although the interest rates of Money Lender are generally higher than banks, compared with banks which normally take 1-6 weeks for examining procedure, the process of Money Lender is more simplified[7]. Continue reading →

This is a guest post by Pawee Jenweeranon, a graduate school student of the program for leading graduate schools – cross border legal institution design, Nagoya University, Japan. Pawee is a former legal officer of the Supreme Court of Thailand. His research interests include internet finance and patent law in the IT industry.

1. Introduction

In the recent years, it is inevitable that the financial technology or Fintech takes the significant role toward the evolution of financial services industry in this region. In other words, Fintech normally be used to improve the financial industry services.

In 2015, the Monetary Authority of Singapore (hereinafter referred to as “MASâ€) has committed two hundred twenty five million Singapore Dollar (around 166 million USD) to support the development of Fintech industry for the startup ecosystem in the upcoming years[1]. This is a good reflection of the significance of the financial technology or Fintech development in Singapore.

From the economic perspective, Small and Medium Enterprises (hereinafter referred to as “SMEsâ€) are important part of Singapore’s economy. SMEs account for 99 percent of all registered enterprises in Singapore[2]. From this reason, enhancing the competitive capacity of Singapore SMEs is essential for Singapore economy development.  Even almost all of the SMEs in Singapore are supported by the Governmental Enterprise Development Agency and Centers[3], (more than 100,000 SMEs got funding support by the Singapore government[4]); however, internet financial technology was also proposed as an alternative mechanism for enhancing the competitiveness of Singapore SMEs in the recent years[5].

2. Regarding Peer to Peer Lending

2.1 Background Generally, there are many peer to peer lending platforms in Singapore; however, they normally lend money to businesses rather than individuals due to the strict regulation for money lenders. The additional limitation on lending to low-income borrowers[6] who are Singaporean citizens or permanent residents which is another requirement should be considered by the lenders.

In general, money lending in Singapore is mainly regulated by the Moneylenders Act 2010 and the Moneylenders Rules 2009. For the Moneylenders Act 2010, due to the main purpose of this act is to develop consumer protection mechanism to protect borrowers of small amount loans[7], this is the reason why the act provides stringent limitation for moneylenders to operate their business. This is another key different of money lending law of Singapore compared to other countries in Asia such as Hong Kong which focusing more on lending activity[8]. Briefly, the act requires moneylenders to hold the Moneylenders license with obligations and limitations for licensee[9].

In Singapore, even there are strict regulations in the existing law relating to a money lending business; however, there is the legislative effort of the Singapore government to address the issue regarding Securities-based Crowdfunding, which can reflect the understanding of the Singapore government toward the development of Financial Technology (Fintech) and the supporting regulatory framework.[10]

2.2 TheRegulatory Framework for Peer to Peer Lending Business

From the document published by the MAS on Lending-based Crowdfunding – Frequently Asked Questions (FAQs)[11], generally, the operation of P2P lending is restricted by MAS under the Securities and Futures Act (Cap. 289) (SFA) and the Financial Advisers Act (Cap. 110) (FFA).

Specifically, the P2P lending business needs to prepare and register a prospectus with MAS in accordance with Section 239(3) of the SFA. In addition, not only the registration of the prospectus but also the P2P lending platform need to follow the licensing requirements, particularly, the P2P lending business which fall within the scope provided by MAS needs to hold a Capital Market Services (CMS) license. Continue reading →

This is a guest post by Kylie Greeff of whitelabelcrowd.fund

As one of the first countries in Asia to publish a regulatory regime, Malaysia is opening up to entrepreneurs, institutions and global operators to facilitate the ease of business credit through P2P lending. Ranked 18th on the World Banks’ Ease of Doing Business league tables, Malaysia is positioning itself as the conduit for global players to setup in Kuala Lumpur as gateway for serving P2P lending markets across Asia. Malaysia has one of the highest levels of financial inclusion in the world at 92 per cent and the country has taken advantage of mobile phones and online banking to expand access. The recently published Securities Commissions (SC) of Malaysia’s rules on the operation of a Peer-to-Peer platform sets out the minimum requirements for the compliant operation of a Loan based crowdfunding platform in Malaysia.

Given the recent publication of the SC’s rules, we have undertaken a comparison of the regulatory requirements imposed on Malaysian P2P platforms with their UK counter parts. The comparison highlights a number of differences first both in the rules that must be followed to operative a platform as well as the minimum standards imposed on operators operating the platforms in Malaysia. Whilst the comparison identifies a number of differences between the two bodies of regulation, this is not unexpected give the differences in maturity of the two markets. P2P in its earliest form began in 2005 in the UK, with the UK regulator announcing its intention to regulate the sector in 2013. The UK’s early P2P regulations were very similar to those now produced by the SC.

The SC in their production of their regulations have clearly done their research into the rules implemented by many platforms and regulators around the world in helping them draft their first guidelines, and have arguably used the UK’s regulations as their closest reference. A strategy that appears to have been widely adopted in their regulation of other financial markets as well. Below is a more detailed review of the UK and Malaysian regulation.

Capital Requirements

The first noticeable difference in the platform operator rules is the requirements by the SC for a platform to have a minimum paid-up capital of RM5 million (approx. £80,000). The UK regulatory body the Financial Conduct Authority (FCA) does not impose a minimum capital requirement for the start-up of a platform. The FCA instead imposes a capital adequacy Requirement (CAR) on platforms once they are trading and authorised by the regulator. A platform’s CAR requirement is based on the trading performance of the platform weighed against its loan book. The SC’s decision to incorporate a minimum capital level on start-up platforms could be seen as a possible reaction to the recent debate in the UK and USA about the possible implementation of Capital requirements on P2P platforms similar to those currently applicable to banks. This being said, the requirement of RM 5m is not prohibitively high and may not be seen by many market entrants as a particularly high barrier to entry, particularly by those supported by financial institutions familiar with far more prohibitive capital requirements.

Whilst the FCA does not have a start-up paid up capital requirement, recent feeling and expectation in the UK is that the FCA will potentially move to more onerous Capital Requirements similar to those imposed on many other financial institutions.

Investor Communication and Transparency

It is interesting to note that the SC has decided to enforce a specific requirement on P2P operators to use ‘an efficient and transparent risk scoring system’ and to ‘carry out a risk assessment on issuers’. The FCA imposes no such requirement on platforms, although the majority of platforms do incorporate a risk rating identification system for the benefit of lenders, the platforms do not openly publish their system or processes as these are closely guarded as valuable IP of the platforms. In the absence of a specific requirement to have an ‘efficient and clear risk scoring system’ the FCA would expect platforms to assess their market and client needs and ensure that they operate with in the FCA’s Principles for Business (PRIN), most notably in regard to risk modelling, Principles 5,7 and 9. It’s worth noting here that the SC operate similar principles in terms of Fund Management Companies, see Guidelines On Compliance Function For Fund Management Companies.

The language used by the SC of ‘efficient and transparent’ is surprisingly vague and may be intentionally left as such to allow platforms the space to develop naturally allowing the SC room to review practices and later set what they deem to be appropriate transparent and efficient processes.

In its list of Operator Obligations, the SC appears intent on ensuring that the platform operators acknowledge and respond to the need to maintain transparency between the investors and the Issuers and to make investors aware of the nature of their investment. This can be seen in rules 13.05 (d-f). Interestingly rule 13.05 (d) requires operators to ‘carry out investor education programmes’. The FCA again poses no requirement on platforms to ‘educate’ their investors but it does impose standards of disclosure and business conduct in its Handbook. The FCA expects platforms to take measures to ensure that they are open and transparent about the nature of the investment products it offers and that information is clearly displayed and prominent for investors (COBS 2.2.1 and 2.2.2).

Carrying out educational programmes in the form of video’s and blog post as well as informative events are a good way to encourage a higher level of customer engagement, but also goes a long way to building the trust of investors in the platform. Rebuildingsociety.com has benefited greatly from publishing a number of blogs about its journey, the types of investment it offers, the internal processes it uses to ensure the efficient and safe operation of the platform. Transparency is greatly valued by both the investors and the regulators.

Anti-Money Laundering and Financial Crime Prevention

As expected, the SC has incorporated the need and responsibility of platforms to ensure that they carry out sufficient Anti Money Laundering (AML) and Financial Crime (FC) Prevention practices as part of their normal operating processes. AML and FC are increasingly sensitive areas. Whilst the SC’s Guidelines on Recognized Markets does not set out specific instructions and guidance on the expected processes and levels of due diligence required by platforms, platforms should look to the SC’s ‘Guidelines On Prevention Of Money Laundering And Terrorism Financing For Capital Market Intermediaries’ which was developed from Section 83 and section 66E of the Anti-Money Laundering and Anti-Terrorism Financing Act 2001 (AMLATFA) and section 377 of the Capital Markets and Services Act 2007 (CMSA). This document sets out the SC’s expectations of platforms in relation to AML and FC prevention.

The SC’s guidelines on AML and FC prevention are broadly similar to those of the FCA set out in SYSC 6.3, in that advocate a risk based, profiling approach to AML and FC prevention processes and require firms to incorporate enhanced Due Diligence practices where individuals are profiled to be higher risk. Continue reading →